Did you know that missing one specific six-month window could mean being denied coverage or paying 40% more for your health insurance? Many Florida seniors mistakenly wait for the October 15th Annual Enrollment Period to shop for Medigap, only to find they’ve already missed their best opportunity. Understanding exactly when does medicare supplement open enrollment take place is the only way to ensure you aren’t forced to undergo medical underwriting or pay higher premiums due to pre-existing conditions.

It’s understandable to feel overwhelmed by the constant pressure from national call centers and the confusing overlap between different federal deadlines. You deserve the peace of mind that comes from making an informed decision for your 2026 health plan. This guide provides a clear timeline for your specific situation so you can lock in the best rates available in the Sunshine State. We will break down your Florida “Guaranteed Issue” rights and show you how a local Jensen Beach licensed agent can provide a no-obligation review of your options.

Key Takeaways

- Identify exactly when does medicare supplement open enrollment take place to secure your coverage without the stress of medical underwriting or health questions.

- Learn how your Medicare Part B enrollment triggers a critical six-month window and the specific steps to take if you are still working in Florida.

- Discover Florida-specific “Guaranteed Issue” rights that offer peace of mind for Treasure Coast residents transitioning between different types of coverage.

- Understand the long-term financial risks of missing your deadline, including how certain health conditions could impact your eligibility for competitive rates.

- See how a no-obligation review with a local Jensen Beach licensed agent provides a clear comparison of various top-rated Florida Medicare Supplement carriers.

Understanding the 6-Month Medigap Open Enrollment Period in Florida

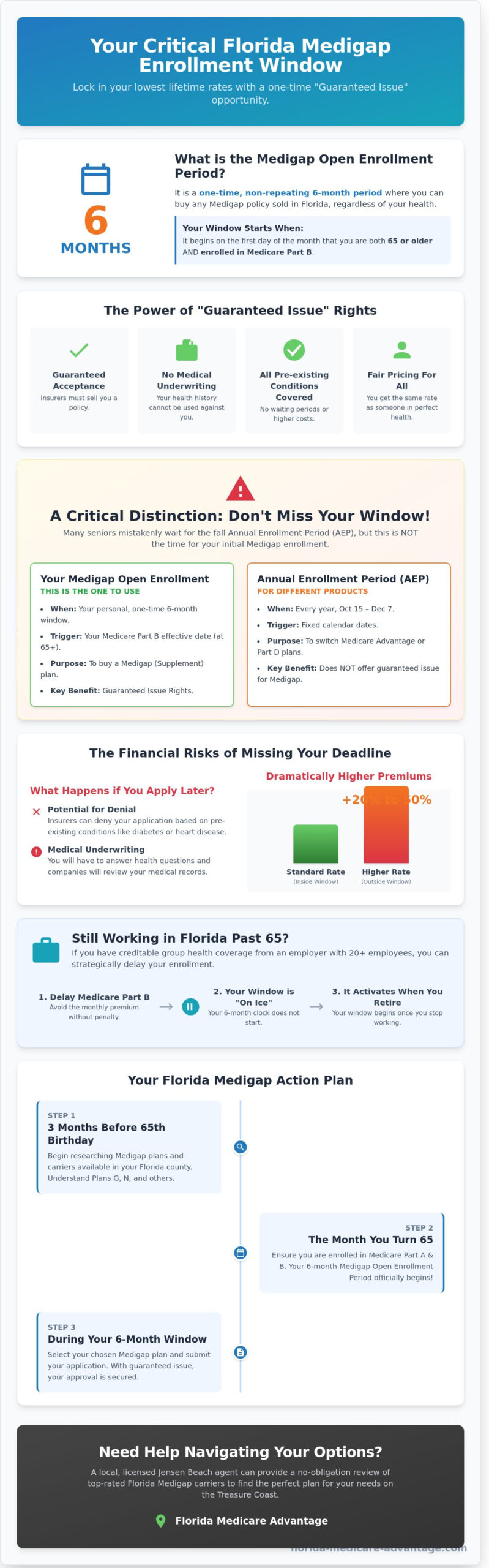

Choosing the right time to secure extra health coverage is a critical decision for Florida retirees. Many seniors ask, when does medicare supplement open enrollment take place? The answer is specific to your personal history rather than a fixed calendar date. Your Medigap Open Enrollment Period is a one-time, 6-month window. It begins the first day of the month you’re 65 or older and enrolled in Medicare Part B. During this timeframe, you have a “guaranteed issue” right. This means private insurance companies can’t use medical underwriting to deny you coverage or charge higher premiums based on your health history. They must accept your application for any Medigap policy they sell at the same rate as someone in perfect health. This window is the most vital opportunity to lock in lower rates for the rest of your life.

The Difference Between AEP and Your Personal Medigap Window

Confusion often arises because of the high volume of advertisements sent during the fall. The Annual Enrollment Period (AEP) runs from October 15 to December 7 every year. This window is designed for changing Medicare Advantage or Part D prescription plans. It’s not the primary time for Supplement enrollment. Your 6-month Medigap window is a personal timeline triggered by your Part B enrollment, independent of the fall Annual Enrollment Period. If you wait for the October window to buy a Supplement for the first time, you might already be outside your protected 6-month period. Understanding when does medicare supplement open enrollment take place for your specific situation prevents costly mistakes.

Why Timing is Everything for Florida Seniors

Florida hosts over 4.8 million Medicare beneficiaries, creating a high-demand market where timing affects your wallet directly. If you miss your initial 6-month window, Florida insurers can legally look at your medical records. They might charge you 20% to 50% more in monthly premiums than they would have during your open enrollment. In some cases, they can deny coverage entirely for pre-existing conditions like diabetes or heart disease. For residents in Jensen Beach and across the Treasure Coast, planning starts early. Local experts recommend reviewing your options 3 months before your 65th birthday. This proactive approach ensures your coverage is active the moment your Part B starts, providing immediate peace of mind and long-term financial security.

- Guaranteed Issue: No health questions asked during the first 6 months of Part B.

- Rate Stability: Locking in a plan early helps avoid the steep price hikes associated with medical underwriting.

- Local Advantage: Florida’s unique regulations mean your timeline is your greatest asset in a competitive market.

How Medicare Part B Triggers Your Supplement Enrollment Window

The timing of your Medigap journey depends entirely on one specific date: your Medicare Part B effective date. While Part A covers hospital stays, Part B handles your doctor visits and outpatient services. You must have both active to secure a Supplement plan. Understanding exactly when does medicare supplement open enrollment take place is the first step toward long-term financial security. This six-month window officially begins on the first day of the month you are both age 65 or older and enrolled in Part B.

If you miss this window, you may face medical underwriting. This process allows insurance companies to review your health history and potentially charge higher premiums or deny coverage. In Florida, securing your plan during this initial period ensures you get the best possible rates regardless of your health status. It’s a one-time opportunity to bypass health questions entirely.

Enrolling While Still Working in Florida

Many Florida residents continue working past age 65. If your Florida-based employer has 20 or more employees, your group health insurance is typically considered primary. You can often delay Part B without penalty. This delay is strategic. It keeps your Medigap enrollment window “on ice” until you actually need it. Once you leave that job or the coverage ends, you have a 63-day window to enroll in certain Medigap plans under guaranteed issue rights. It’s vital to ensure your employer coverage is “creditable,” meaning it’s at least as good as Medicare’s standard. A local expert can review your current benefits to confirm if delaying Part B is your best financial move.

The Automatic Start: When You Don’t Have to Do Anything

If you already receive Social Security benefits at least 4 months before turning 65, the government automatically enrolls you in Parts A and B. Your red, white, and blue Medicare card will arrive in your mailbox about 12 weeks before your birthday. Check the lower right corner of this card. It lists your Part B effective date. This date is the “starter pistol” for your enrollment window. Don’t let this date surprise you. An “accidental” start can cause your Medigap window to expire before you’ve even compared plans. Always verify your specific effective dates on your Notice of Award letter. This ensures you know exactly when does medicare supplement open enrollment take place for your specific situation.

Florida-Specific Guaranteed Issue Rights & Moving to the Treasure Coast

Relocating to the Treasure Coast often changes your healthcare options immediately. Many seniors ask when does medicare supplement open enrollment take place only to discover that a move to Martin County provides a unique entry point. Guaranteed Issue (GI) rights act as a vital safety net. If you lose your previous coverage because you moved out of the service area, insurance companies must sell you a Medigap policy. They can’t charge you more for pre-existing conditions or deny you coverage. This protection is essential for Jensen Beach residents who previously relied on regional HMOs in other states.

Moving to Florida: Your Medigap ‘Reset’ Button

Relocating from a state like New York to Florida triggers a 63-day window to secure a Medigap plan. This happens because your old Medicare Advantage plan likely doesn’t operate in the Florida market. To qualify, you need a disenrollment letter from your previous carrier as proof of your move. Contacting a Jensen Beach agent within 30 days of your move ensures you don’t face a gap in coverage. Local experts help you transition from a restrictive HMO to the freedom of a Florida Medigap plan without any medical underwriting.

Trial Rights and Switching Plans in Florida

Florida seniors have a 12-month Trial Right when testing Medicare Advantage for the first time. If you decide the plan isn’t a fit within the first year, you can return to Original Medicare and buy a Medigap policy. This protection includes switching between popular options like Plan G and Plan N. While national call centers might rush your decision, local licensed agents understand the specific carrier rules in Florida. You generally have 60 days after your Advantage plan ends to pick your new supplement. Understanding when does medicare supplement open enrollment take place is much easier when you have a steady neighbor guiding the process.

- 63 Days: The standard window to apply for a Medigap plan after losing other health coverage.

- 12 Months: The duration of your Trial Right if you are new to Medicare Advantage.

- 0 Medical Questions: Guaranteed Issue rights mean you skip the health questionnaire entirely.

Our team provides a no-obligation review to help you document your move correctly. We ensure your paperwork reaches the carrier before your 63-day window closes. This proactive approach secures your peace of mind while you settle into your new Florida lifestyle.

Of course, settling into a new lifestyle involves more than just healthcare. Along with finding a home with firms like Morgan Property Solutions Inc., it’s wise to review your auto coverage for the Florida market. To get started on that front, you can discover SI Insurance.

What Happens if You Miss the Medicare Supplement Deadline?

Missing your initial window creates a significant shift in how you access coverage. Understanding when does medicare supplement open enrollment take place is vital because this six-month period is the only time Florida carriers must accept you regardless of your health. Once this window closes, the “guaranteed issue” protection disappears. You’re then subject to medical underwriting, which allows insurance companies to scrutinize your medical records before deciding to offer a policy.

Florida seniors who apply late often face higher monthly premiums or outright denials. Common conditions that lead to immediate rejection in the Sunshine State include congestive heart failure, Parkinson’s disease, or a recent stroke within the last 24 months. If a carrier does accept you despite a pre-existing condition, they may implement a 6-month waiting period. During this time, the plan won’t pay for costs related to that specific health issue, leaving you responsible for those expenses out of pocket.

The Medical Underwriting Process in Florida

In Florida, medical underwriting for Medigap involves a review of your 2-year medical history and current prescriptions to determine your eligibility and rate. Major carriers like Florida Blue or UnitedHealthcare will require you to complete a detailed health questionnaire. They look specifically for chronic medications or upcoming surgeries. Your physical build also matters; many Florida insurers use strict height and weight charts. If your Body Mass Index (BMI) falls outside their accepted range, you could face a “rated” policy with a 15% to 25% surcharge. Tobacco users in Florida should also expect to pay significantly more, with some premiums jumping 10% higher than non-smoker rates.

Strategic Alternatives if You Are Denied

Don’t lose hope if a Medigap carrier denies your application. You have other paths to secure comprehensive care. Florida Medicare Advantage plans (Part C) serve as a powerful fallback because they don’t use medical underwriting for enrollment. These plans often include extra benefits like dental and vision that standard Medigap plans lack. You might also qualify for a “Guaranteed Issue” event if your current Medicare Advantage plan leaves your Florida county or if you lose employer-sponsored health coverage. These specific events grant you a 63-day window to join a Medigap plan without answering a single health question.

A professional review can help you identify carriers with more lenient standards. Some smaller insurers in Florida may overlook certain stable health conditions that larger national brands reject. Our licensed agents can compare these underwriting guidelines to find a match for your specific situation. If you’ve missed your initial window, schedule a no-obligation review to explore your remaining coverage options today.

Navigating Florida Medigap Plans with a Local Jensen Beach Expert

Selecting the right health coverage shouldn’t feel like a gamble. While national 1-800 call centers often rely on generic scripts, a local Jensen Beach expert understands the specific healthcare landscape of the Treasure Coast. We provide a side-by-side comparison of top-rated carriers like Humana and Florida Blue, focusing on how their rate stability affects your long-term costs. Because Florida’s insurance market is unique, having a licensed agent who lives in your community ensures you aren’t just another number in a database.

A common question we hear is, when does medicare supplement open enrollment take place? For most, this six-month window begins the first day of the month you’re both 65 or older and enrolled in Medicare Part B. During this time, you have a guaranteed issue right. This means insurance companies can’t deny you coverage or charge more for pre-existing conditions. Our “No-Obligation” review is a free service for consumers. Licensed agents are compensated by the carriers, so you receive professional guidance without a consultation fee.

As we prepare for 2026, anticipating rate changes is vital. Florida’s Medigap premiums can fluctuate based on inflation and healthcare utilization trends. By reviewing your plan now, we can identify if a different carrier offers the same standardized benefits at a more competitive price point. For a comprehensive overview of all your options, including Medicare Advantage plans with dental and vision benefits, you can explore our Florida Medicare guide for 2026 that compares plans and enrollment options.

Why Local Knowledge Matters in Martin County

Healthcare is personal and local. Our expertise extends beyond plan codes to real-world applications in the Jensen Beach area:

- Provider Access: We identify which local specialists and Jensen Beach doctors accept specific Medigap and Part B combinations to ensure your care remains uninterrupted.

- Personalized Service: You can skip the automated phone menus and visit us for a face-to-face consultation right on NE Jensen Beach Blvd.

- Administrative Relief: We handle the “paperwork headache” from start to finish. Our team ensures your application is filed correctly with the carrier at no cost to you.

Your Next Steps: Securing Your 2026 Coverage

The timeline for your 2026 application is closer than you think. It’s best to start your review at least 90 days before your target effective date. This buffer allows you to compare the latest rate filings and ensure your preferred doctors are still in the network. Before your appointment, gather your current medication list and a list of your primary physicians.

Understanding when does medicare supplement open enrollment take place is the first step to securing your financial future. Don’t wait until the last minute to explore your options and potentially miss out on lower premiums. We’re here to provide the clarity you need to make an informed decision about your health.

Secure Your Coverage During Your Florida Medigap Window

Navigating your 6-month Medigap window requires precision because this one-time opportunity doesn’t reset. You’ve learned that the first day of your Medicare Part B effective month triggers your enrollment period. Missing this 180-day window often means facing medical underwriting or higher monthly premiums. If you’ve recently moved to Jensen Beach, you might also qualify for Florida-specific Guaranteed Issue Rights that protect your ability to switch plans without health questions. Understanding exactly when does medicare supplement open enrollment take place is the first step toward long-term financial security.

Our team provides 100% no-obligation plan comparisons to help you evaluate the 10 standardized Medigap options available in 2026. We’re local experts who understand the specific regulations governing Florida’s insurance market. Don’t leave your supplemental coverage to chance or a national call center. You can Speak with a Licensed Florida Medicare Agent in Jensen Beach today to review your eligibility and lock in your benefits. We’re here to ensure you find the right plan with the professional clarity you deserve.

Frequently Asked Questions

Can I change my Medicare Supplement plan at any time in Florida?

You can apply to change your Medicare Supplement plan at any time in Florida, but you’ll usually have to pass a health screening. Unlike Medicare Advantage, Medigap doesn’t have a restricted annual window for switching. If you apply after your initial 6-month period, carriers can deny coverage based on pre-existing conditions. A licensed agent can help you compare 10 different carriers to find a plan that accepts your health history and offers lower premiums.

Is there an Annual Open Enrollment period for Medigap in Florida?

No, there’s no annual open enrollment period for Medigap plans in Florida. Many seniors confuse the October 15 to December 7 window with Medigap, but that period only applies to Medicare Advantage and Part D plans. If you’re wondering when does medicare supplement open enrollment take place, it’s a one-time, 6-month window that begins the month you’re 65 and enrolled in Part B. Once that window closes, you lose your guaranteed right to buy a policy.

What is the 6-month rule for Medigap insurance?

The 6-month rule refers to your one-time Medigap Open Enrollment Period that starts the day your Medicare Part B coverage begins. During these 180 days, insurance companies must sell you any policy they offer at the best available rate regardless of your health. They can’t charge you more for chronic conditions like diabetes or heart disease. Missing this window means you’ll likely face medical questions and potential denial from 100 percent of private insurers.

Do I have to re-enroll in my Medigap plan every year?

You don’t have to re-enroll in your Medigap plan each year because these policies are guaranteed renewable. As long as you pay your monthly premiums, the insurance company can’t cancel your coverage or change your benefits. Your plan will automatically stay active on January 1 without any paperwork. This provides long-term peace of mind for Martin County residents who want consistent coverage without the stress of annual shopping or changing networks.

What happens to my Medigap window if I move to Jensen Beach from another state?

Moving to Jensen Beach doesn’t trigger a new 6-month open enrollment window, but you can usually keep your current policy. Since Medigap is portable, your coverage follows you across state lines. However, Florida’s 67 counties have different premium rates, so your monthly cost might change. You should request a no-obligation review from a local expert to see if a Florida-based carrier offers a lower rate for your new 34957 zip code compared to your previous state.

Can a Florida insurance company cancel my Medigap policy if my health changes?

A Florida insurance company cannot cancel your Medigap policy because of changes in your health status. Federal law requires these plans to be guaranteed renewable, which protects you even if you develop a serious illness after enrollment. Your coverage remains secure as long as you continue to pay your premiums on time. This protection ensures that your 20 percent coinsurance gaps remain covered regardless of any new medical diagnoses or increased usage of healthcare services.

How much does a Medicare Supplement plan cost in Florida for 2026?

For 2026, a 65-year-old non-smoker in Florida can expect to pay between $180 and $260 per month for Plan G. Prices fluctuate based on your specific zip code, age, and gender. While the benefits for Plan G are standardized by the government, premiums can vary by 30 percent between different carriers. Speaking with a local expert allows you to compare 12 different insurance companies to ensure you aren’t overpaying for the same mandated benefits.

Is Plan G or Plan N better for seniors living in Martin County?

Plan G is often the top choice for Martin County seniors who want 100 percent coverage of their out-of-pocket costs after the Part B deductible. Plan N is a budget-friendly alternative that can save you $30 to $50 per month in premiums. However, Plan N requires small copays of up to $20 for office visits and $50 for emergency room trips. If you prefer fixed costs and zero copays, Plan G provides the most financial certainty.