What if the 12 different marketing flyers sitting on your kitchen table right now are actually preventing you from making the best choice for your health? For many Treasure Coast residents, the sudden influx of national advertisements for florida medicare feels more like a burden than a benefit. You want to ensure your regular doctor at Cleveland Clinic Martin North stays in your network, but the fine print in those brochures is often intentionally vague. It’s natural to feel anxious about how premiums and co-pays will impact your fixed income in 2026.

You deserve a clear path to the benefits you’ve earned. This guide simplifies the 2026 options by comparing Medigap and Advantage plans specifically for Jensen Beach neighbors. We’ll show you how to find a plan that includes dental, vision, and SilverSneakers while protecting your access to local specialists. You’ll learn exactly how to transition into your new coverage with a stress-free enrollment process guided by local expertise.

Key Takeaways

- Compare out-of-pocket costs and provider networks to determine if a low-premium Advantage plan or a flexible Medigap policy fits your lifestyle.

- Access our criteria-based ranking to identify the top-rated 2026 carriers specifically serving Martin County and the Treasure Coast.

- Master the 2026 florida medicare roadmap to ensure you never miss critical enrollment deadlines or lose access to essential benefits.

- Discover why partnering with a local Jensen Beach agent provides a level of personalized service and plan choice that national call centers cannot match.

- Learn how to navigate the unique density of regional plan options to secure extra benefits and long-term peace of mind.

Understanding Florida Medicare Options in 2026

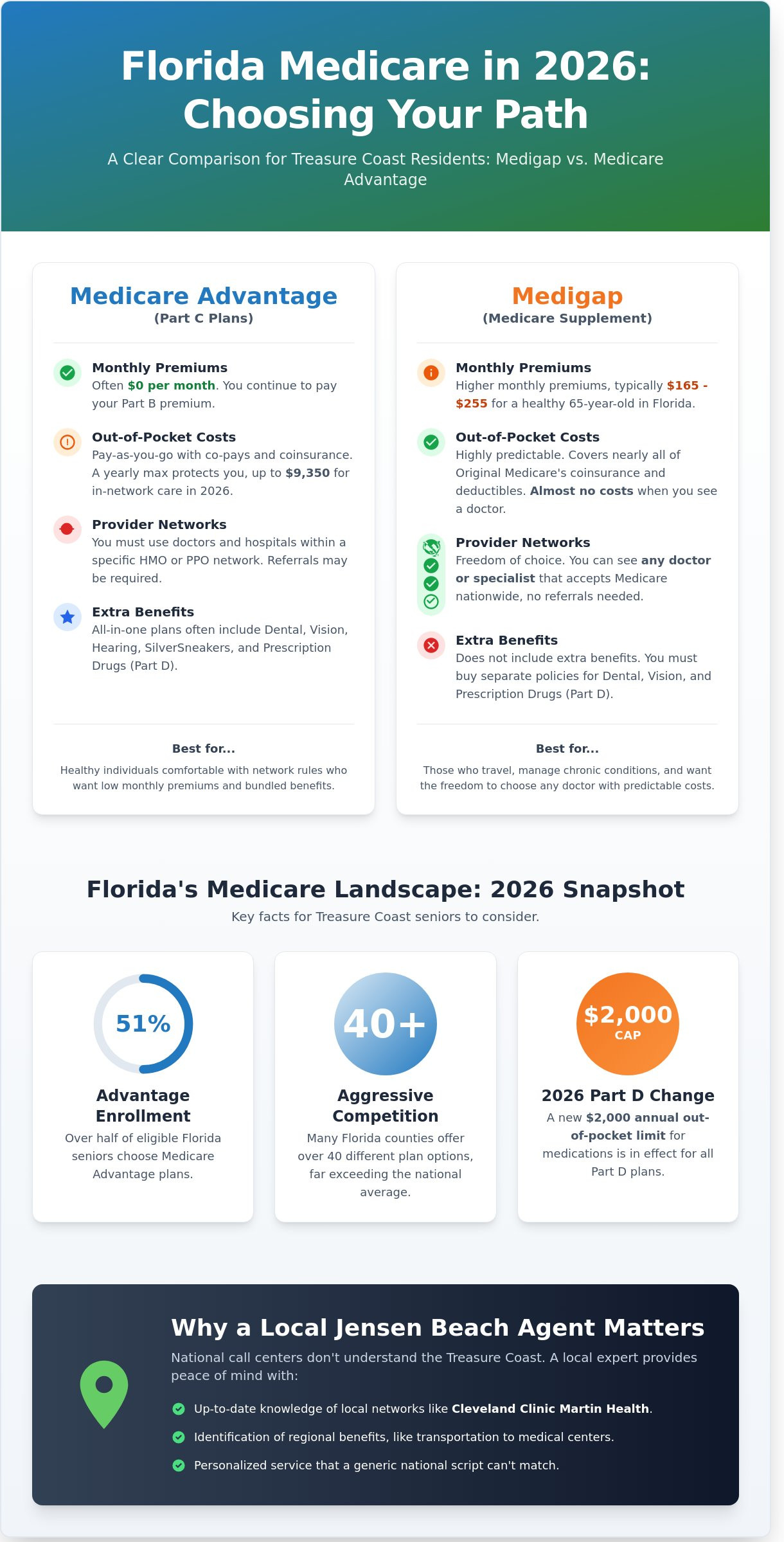

Florida medicare operates as a unique marketplace characterized by high competition and a vast array of choices. In 2026, the landscape shifted due to federal regulations that redesigned Part D prescription drug benefits. One major change is the $2,000 annual out-of-pocket limit for medications. This cap forces residents to re-evaluate their current coverage to ensure their preferred pharmacies remain in-network. Florida consistently ranks among the top states for Medicare Advantage enrollment, with over 51% of eligible seniors choosing private plans over the federal program as of late 2024.

Distinguishing between Original Medicare and private alternatives is your first step toward total health security. Original Medicare provides a foundation through Part A and Part B, but it often leaves gaps in coverage that can lead to high medical bills. Private Florida Medicare Advantage plans often fill these gaps by bundling hospital, medical, and drug coverage into a single package. Choosing the right path requires a clear understanding of how these options differ in 2026:

- Cost structures: Original Medicare has standard deductibles and a 20% coinsurance rate with no out-of-pocket maximum.

- Network rules: Advantage plans typically use HMO or PPO networks restricted to specific Florida providers.

- Additional benefits: Private plans often cover hearing, dental, and vision services that the federal government does not.

The Role of Private Carriers in Florida

Private carriers like Florida Blue, UnitedHealthcare, and Humana dominate the regional market. These companies receive federal funding to provide your benefits. Because Florida has a high concentration of retirees, these carriers compete aggressively for your enrollment. This competition results in a high number of $0 premium plans. In fact, many Florida counties offer over 40 different Medicare Advantage options, far exceeding the national average. These plans often include “extra” benefits like fitness memberships and grocery allowances for those who qualify. Our licensed agents provide a no-obligation review to see which carrier matches your specific prescriptions and budget.

Why Jensen Beach Seniors Need a Local Perspective

National call centers often miss the nuances of the Treasure Coast. For seniors in Jensen Beach, network access is the most critical factor. A local licensed agent understands which plans include Cleveland Clinic Martin Health or local specialists along US-1. National providers might list a doctor as “in-network” when their local status changed as recently as last month. Local experts also identify regional benefits, such as specialized transportation to medical centers in Stuart or Port St. Lucie. Working with a neighbor ensures your plan works where you actually live. It’s about finding peace of mind through local expertise rather than a generic national script.

Florida Medicare Advantage vs. Medigap: Which is Right for You?

Choosing the right florida medicare path involves a clear look at your budget and how you prefer to access healthcare. In 2026, the financial difference between Medicare Advantage and Medigap remains significant. Medicare Advantage plans often feature $0 monthly premiums, but they require you to pay as you go through co-pays and co-insurance. For 2026, the maximum out-of-pocket limit for these plans can reach up to $9,350 for in-network services. Conversely, Medigap plans require a monthly premium, often ranging from $165 to $255 for a healthy 65-year-old in Florida, but they cover almost all your out-of-pocket expenses for Medicare-approved services.

Your current health status is the most reliable guide for this decision. If you manage chronic conditions that require frequent specialist visits or diagnostic testing, the predictability of a Supplement plan is invaluable. You can compare Medicare Supplement plans to see how they provide long-term cost stability regardless of how often you visit the doctor. For those who are generally healthy and prefer a lower monthly fixed cost, the bundled approach of Medicare Advantage might be the better fit. The tradeoff is simple: you either pay more upfront for total freedom or pay less monthly for a managed network of care.

The Pros and Cons of Medicare Advantage in Florida

Florida Part C plans are famous for “extra” benefits that Original Medicare does not cover. In 2026, many Florida residents will see expanded dental, vision, and hearing coverage, along with monthly over-the-counter allowances for health supplies. However, you must stay within a specific network. In areas like the Treasure Coast, an HMO (Health Maintenance Organization) typically requires you to choose a primary care physician and obtain referrals for specialists. A PPO (Preferred Provider Organization) offers more freedom to see doctors outside the network, though your costs will be higher. You can explore our Medicare Advantage plans guide for a deeper analysis of how these networks function in your specific county.

The Stability of Medicare Supplement (Medigap) Plans

Many Florida seniors choose Medigap Plan G because it offers total freedom. You can see any doctor in the United States who accepts Medicare; no referrals are ever required. Florida’s market is unique because of its rating systems. Many plans here use “Issue Age” or “Community Rated” pricing. This means your premium is not hiked simply because you had a birthday; increases are usually tied to medical inflation instead. Remember that Medigap does not include prescription coverage. You will need to pair your supplement with a standalone florida medicare Part D plan to ensure your medications are covered. If you’re considering a Medigap policy, understanding the Medicare Supplement open enrollment period in Florida is crucial to securing the lowest rates without medical underwriting. If you have questions about which direction fits your lifestyle, you can always speak with a local expert for a no-obligation review of your options.

Evaluating the Best Medicare Plans in Florida for 2026

Selecting a florida medicare plan requires more than a glance at the monthly premium. You need a reliable framework to separate high-performing options from those that might leave you with unexpected costs. Our ranking tool prioritizes the CMS Star Rating system, which grades plans on a scale of 1 to 5 based on clinical outcomes and member experience. For 2026, we also incorporate local feedback from Martin County residents to ensure the data matches the actual care received at facilities like Cleveland Clinic Martin Health.

Confirming your doctor’s status is the most critical step in your annual review. If you see a specialist in Jensen Beach, don’t assume they’ll remain in-network for the upcoming year. Networks shift. Contracts expire. You can verify your 2026 coverage by using a carrier’s provider search tool or by consulting a licensed agent who can run a comprehensive network check across multiple insurers. You can also see our list of the best Medicare Advantage plans to compare how different carriers rank for the current cycle.

Top-Rated Carriers in the Treasure Coast

Florida Blue remains a dominant force in the Treasure Coast because of its deep regional roots. It’s been serving the state for over 75 years; this longevity translates to one of the broadest provider networks in Martin County. Their 2026 plans emphasize local access, often including more independent physicians than national competitors. This makes them a steady choice for seniors who value long-term doctor-patient relationships.

Humana has tailored its 2026 Florida offerings toward proactive wellness. Many of their plans feature the SilverSneakers program and robust mail-order pharmacy incentives that can reduce monthly costs. UnitedHealthcare provides AARP-branded options that appeal to seniors looking for scale and stability. Their 2026 portfolio in the Treasure Coast focuses on “all-in-one” convenience, often bundling dental, vision, and hearing benefits with low or $0 monthly premiums.

Specialized Plans: D-SNP and C-SNP in Florida

For seniors with unique health or financial needs, specialized florida medicare options provide targeted support. Dual Eligible Special Needs Plans (D-SNP) are available to those who qualify for both Medicare and Medicaid. These plans often eliminate most out-of-pocket costs and provide “extra help” with prescription drugs, which is vital as the $2,000 out-of-pocket cap on medications takes full effect in 2026.

Chronic Condition Special Needs Plans (C-SNP) serve residents managing heart disease, lung conditions, or diabetes. These plans offer specialized provider networks and care coordinators who help manage complex treatment schedules. If you’re on a fixed income, Florida’s state-specific programs can further subsidize your Part B premiums, providing much-needed financial peace of mind. Speaking with a local expert ensures you don’t overlook these specific state-level savings.

Florida Medicare Enrollment: Deadlines and Roadmaps

Success with florida medicare depends on your ability to hit specific dates on the calendar. Missing these windows leads to higher premiums and gaps in your healthcare coverage. The 2026 roadmap begins with the Annual Enrollment Period (AEP). This window runs from October 15 to December 7 every year. During this time, you can join, drop, or switch a Medicare Advantage plan or a Part D prescription drug plan. Your new coverage then begins on January 1.

If you already have a Medicare Advantage plan, the Open Enrollment Period (OEP) offers a second chance. From January 1 to March 31, you can switch to a different Advantage plan or return to Original Medicare. This period is designed for those who find their current plan doesn’t meet their needs after the new year begins. Making a change during OEP ensures you have the right benefits for the remainder of the year.

The Initial Enrollment Period (IEP) for Florida Residents

Your journey often starts with the Initial Enrollment Period. This is a seven-month window centered around your 65th birthday. It includes the three months before you turn 65, your birth month, and the three months following. We recommend using a checklist for those turning 65 and exploring Medicare options to track your progress. If you’re still working for a company with 20 or more employees, you might delay Part B without penalty. You should follow the specific steps for those new to Medicare to coordinate your employer coverage with federal requirements. For those considering Medigap coverage, this initial period is also when you have guaranteed access to Medicare Supplement open enrollment in Florida without medical underwriting.

Special Enrollment Periods (SEP) in Florida

Life in Florida sometimes requires flexibility. A Special Enrollment Period allows you to change your florida medicare coverage outside of standard dates. Qualifying events include moving to a new county in Florida or losing your group health coverage. Usually, you have 63 days from the loss of coverage to enroll in a new plan. Florida residents also gain unique protections during hurricane season. If a FEMA disaster declaration occurs, CMS may grant an SEP for those who were unable to make a selection during a regular window. This provides peace of mind when natural disasters disrupt your planning.

Avoiding permanent late enrollment penalties is vital for your financial security. If you miss your initial window without having creditable coverage, the Part B penalty adds 10% to your premium for every full 12-month period you waited. The Part D penalty is 1% of the national base premium for every month you went without coverage. These costs stay with you for life. Our licensed agents help you navigate these dates to ensure you never pay more than necessary. For a personalized look at your enrollment window, speak with a local expert today.

Why Work with a Local Jensen Beach Medicare Agent?

Choosing a plan through a captive agent limits your options to a single insurance carrier. These agents work for the company, not for you. By contrast, an independent Florida brokerage evaluates multiple carriers simultaneously to find the most competitive rates for 2026. This independence ensures your needs dictate the plan choice, rather than a corporate sales quota. You gain access to a broad spectrum of florida medicare options that a single-company representative simply cannot offer. This model of expert advocacy is similar to how an owner’s representative, like FALKE Atlantic Corporation, champions a client’s interests during a major construction project.

This independent approach is also valuable when securing other forms of financial protection, such as life insurance. Online brokerages like lifeinsure.com allow you to compare quotes from various carriers to find the best fit for your family.

National call centers often lack the regional insight required to understand the Treasure Coast healthcare market. A representative in a different time zone won’t know if your primary care physician in Jensen Beach is still participating in a specific network. Local agents provide a layer of advocacy that national centers cannot match. If you face a claim dispute or a provider network change, your local expert acts as a liaison between you and the insurance company. This personal connection replaces the frustration of automated phone menus with direct, human accountability. We live in the same community, so we understand the local medical landscape intimately.

Personalized Plan Comparisons

Florida Medicare Advantage agents utilize your specific medication list to calculate your total annual out-of-pocket costs. This data-driven approach is essential because florida medicare Part D plans often change their formularies every January. We identify the specific tier for each of your prescriptions to ensure you pay the lowest possible co-pay at your preferred pharmacy. Our office in Jensen Beach offers a quiet, professional space where you can review these details face-to-face. The local advantage is the intersection of federal knowledge and Florida geography. Having a local professional means your plan will actually work at the hospitals and clinics you visit most often.

Your Next Steps for 2026 Florida Enrollment

Preparing for the 2026 enrollment cycle requires a methodical review of your current coverage. You can schedule a no-obligation review to ensure your benefits still align with your health needs. These consultations typically last 45 minutes and provide a clear roadmap for the upcoming year. To make the most of your Jensen Beach consultation, please bring the following items:

- Your red, white, and blue Medicare card.

- A complete list of all prescription medications, including dosages.

- Names and addresses of your primary care doctors and specialists.

- Your current 2025 “Evidence of Coverage” document if available.

Professional Medicare assistance in Florida is always free of charge to the consumer. Licensed agents are compensated by the insurance carriers, which means you receive expert guidance without any added expense or hidden fees. This structure ensures you can focus entirely on your health and peace of mind while we handle the technical details of your enrollment. It’s our goal to ensure every senior in Jensen Beach feels confident and secure in their 2026 coverage choices.

Secure Your Healthcare Future for 2026

Navigating the upcoming changes to florida medicare doesn’t have to be a source of stress. You now understand the vital differences between Medicare Advantage and Medigap, and you’re aware of the 2026 enrollment deadlines that dictate your coverage options. Making an informed decision ensures you protect both your health and your fixed income from unexpected costs. Choosing the right plan today means you won’t face coverage gaps when you need care the most.

Our licensed local agents in Jensen Beach specialize in simplifying this complex process. We’re authorized to offer plans from leading carriers like Humana, UHC, and Florida Blue, giving you access to a wide range of benefits tailored specifically to the Florida market. We provide no-cost, no-obligation consultations to help you compare 2026 premiums and co-pays without any sales pressure. You’ll gain the clarity of a professional review while working with a neighbor who understands our local healthcare landscape and provider networks.

Get Your Free 2026 Florida Medicare Plan Review Today

You’ve earned these benefits through years of hard work. We’re here to help you claim them with confidence and ease.

Frequently Asked Questions

What is the most popular Medicare Advantage plan in Florida for 2026?

UnitedHealthcare remains the most popular provider in the state, serving approximately 1.2 million residents according to recent enrollment data. While popularity varies by county, Humana and Florida Blue also hold significant market shares exceeding 15 percent each. Choosing a plan depends on your specific zip code and your preferred provider network. Our licensed agents can help you compare these top-rated options to find the right fit for your needs.

How do I sign up for Florida Medicare if I am turning 65 this year?

You sign up for Florida medicare through the Social Security Administration during your seven-month Initial Enrollment Period. This window begins three months before you turn 65 and ends three months after your birth month. You can complete your application online at ssa.gov or visit one of the 50 local Social Security offices across the state for in-person assistance. It’s a straightforward process that ensures your coverage begins on the first day of your birth month.

Can I keep my Florida doctor if I switch to a Medicare Advantage plan?

You can keep your doctor if they participate in the specific Medicare Advantage plan’s provider network. Most HMO plans require you to use in-network providers, while PPO plans allow you to see out-of-network doctors at a higher cost. We recommend verifying your physician’s status directly with our local experts to ensure your 2026 coverage remains seamless. Over 90 percent of Florida primary care physicians participate in at least one major Advantage network.

What is the difference between Florida Medicare Part C and Part D?

Florida medicare Part C, known as Medicare Advantage, combines your hospital, medical, and often drug coverage into one private plan. In contrast, Part D is a standalone policy specifically for prescription drugs, often paired with Original Medicare. While Part C acts as an all-in-one alternative, Part D focuses solely on reducing your pharmacy out-of-pocket expenses. Most Florida residents find that Part C offers more comprehensive benefits, including dental and vision care.

Are there zero-premium Medicare plans available in Martin County, Florida?

Yes, Martin County residents have access to 18 different zero-premium Medicare Advantage plans for the 2026 cycle. These plans eliminate the monthly plan premium, though you must continue paying your Part B premium to the federal government. Residents in Stuart and Hobe Sound often choose these options to maximize their fixed income while maintaining comprehensive health benefits. It’s a practical way to secure extra services without increasing your monthly insurance costs.

How does Florida’s ‘Extra Help’ program work for prescription drugs?

The Extra Help program provides an average annual value of 5,900 dollars to help seniors pay for prescription drug costs. If your annual income is below 22,590 dollars as an individual, you may qualify for reduced premiums and lower co-pays at the pharmacy. This federal program ensures that essential medications remain affordable for those with limited financial resources. Our team provides a no-obligation review to see if you meet the eligibility requirements for this assistance.

When is the next open enrollment period for Florida Medicare?

The next Annual Enrollment Period begins on October 15, 2025, and concludes on December 7, 2025. During these 54 days, you can switch from Original Medicare to an Advantage plan or change your current 2026 coverage. Any changes you make during this window will officially take effect on January 1, 2026. It’s the primary time of year to review your benefits and ensure your plan still meets your health goals.

Is SilverSneakers included in most Florida Medicare Advantage plans?

SilverSneakers is included in approximately 94 percent of Florida Medicare Advantage plans as a standard value-added benefit. This program grants you access to over 15,000 participating fitness locations and community classes throughout the state. It’s a popular feature that helps seniors maintain an active lifestyle without the burden of monthly gym membership fees. You’ll find that staying healthy is much easier when your plan covers the cost of your local fitness center.