Did you know that missing a single six-month window could cost you an extra $500 or more in annual premiums for the rest of your life? If you’re like many Florida seniors, your mailbox is likely overflowing with dozens of national mailers this week. It’s frustrating to try and distinguish between Medigap and Medicare Advantage when every flyer claims to be the best option. You deserve clarity instead of high-pressure sales tactics during your medicare supplement open enrollment period.

We’ll help you master this timing to secure the lowest possible rates and guaranteed coverage without ever answering a single medical question. By understanding the specific 2026 regulations in the Sunshine State, you can avoid the fear of medical underwriting and gain true peace of mind. This guide provides a clear timeline for your enrollment, explains unique Florida-specific protections, and compares Plan G and Plan N to ensure you make the right choice for your budget. You’ll finish this article ready to speak with a local expert and finalize your health strategy with total confidence.

Key Takeaways

- Learn how to time your medicare supplement open enrollment perfectly to bypass medical underwriting and secure guaranteed coverage regardless of your health history.

- Discover how Florida-specific regulations protect local residents and which carriers provide the most reliable coverage options within Martin County.

- Compare the comprehensive “Gold Standard” benefits of Plan G against the budget-friendly structure of Plan N to find your ideal balance of protection and value.

- Follow our step-by-step 2026 enrollment checklist to verify your Part B status and secure the peace of mind that comes with professional local guidance.

What is the Medicare Supplement Open Enrollment Period in Florida?

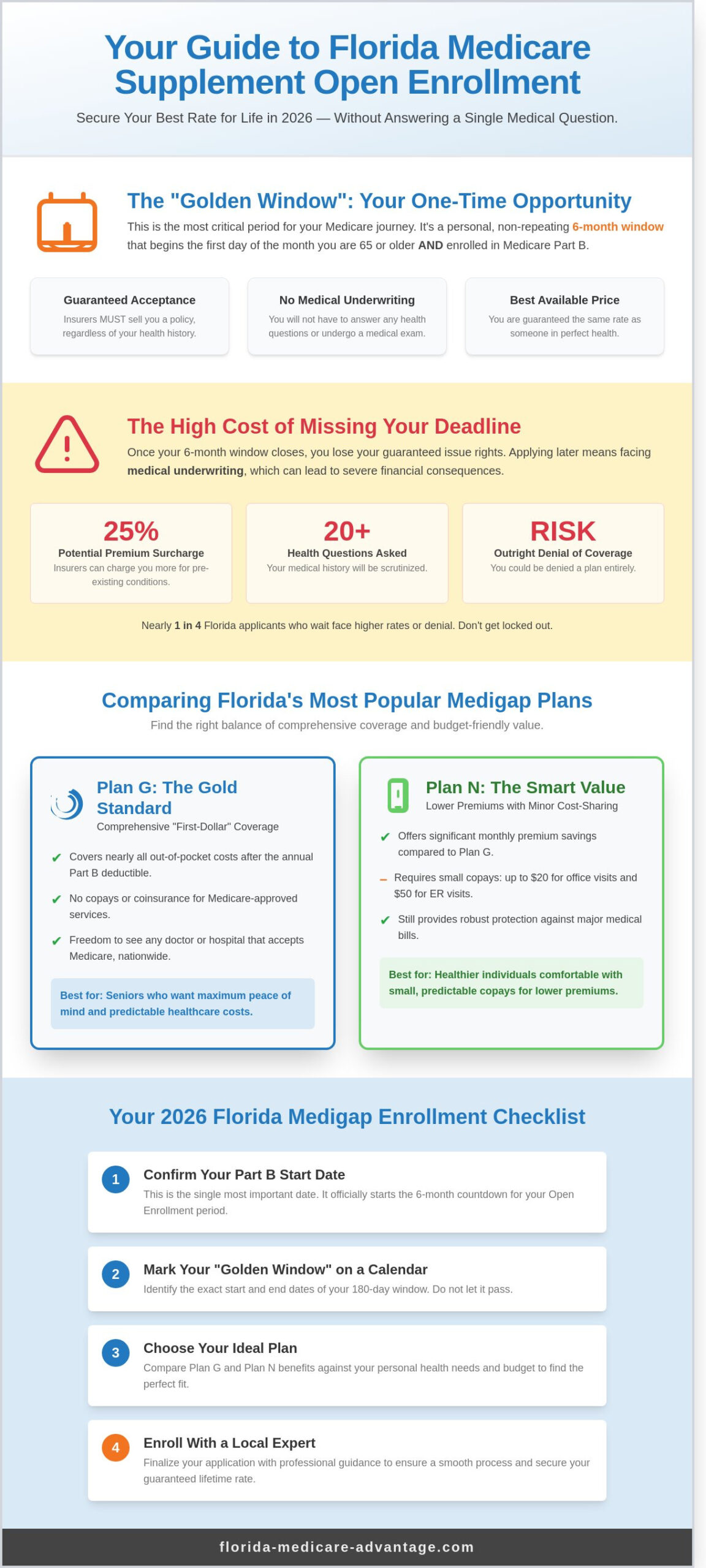

Understanding your medicare supplement open enrollment period is the most critical step in securing your healthcare future in the Sunshine State. This six-month window is unique to your specific situation. It begins the first day of the month you’re 65 or older and enrolled in Medicare Part B. During these 180 days, Florida insurance companies must sell you a policy at the best available rate, regardless of your health history. They cannot deny you coverage or charge higher premiums for pre-existing conditions like diabetes or heart disease.

Florida residents enjoy a distinct advantage during this timeframe. Our state’s large retiree population has fostered a competitive market with dozens of private carriers. A Medigap policy helps pay for costs that Original Medicare doesn’t cover, such as coinsurance and deductibles. You shouldn’t confuse this personal window with the Annual Election Period (AEP) that runs from October 15 to December 7. While AEP is heavily advertised on television, it primarily involves Medicare Advantage and Part D changes. Your Medigap enrollment is a personal milestone, not a national calendar event.

To better understand how this specific timeline works for you, watch this helpful video:

The “Golden Window”: Why timing is everything

The medicare supplement open enrollment window is often called the “Golden Window” because it’s a one-time opportunity for most seniors. Once the 180-day clock starts ticking on your Part B effective date, it doesn’t stop. You cannot “reset” this period later in life if you decide you want a different plan. If you miss this timeframe, you’ll likely have to answer medical questions to qualify for coverage in the future. In Florida, nearly 25% of applicants who wait until after their open enrollment period face higher rates or outright denials due to health issues.

Medigap vs. Medicare Advantage enrollment

It’s vital to distinguish between these two paths. This specific enrollment window applies only to Supplement plans, not Medicare Advantage. While Advantage plans often have lower monthly premiums, a Supplement plan protects your future flexibility. You’ll have the right to see any doctor in Florida, or anywhere in the country, who accepts Medicare. If you’re new to Medicare, choosing a Supplement now ensures you won’t be locked into a provider network. This choice provides peace of mind for those who travel between Florida and other states or prefer specialized specialists at major medical centers.

Guaranteed Issue Rights: Buying Medigap Without a Health Check

Your Medigap Open Enrollment Period is a one-time, six-month window that starts the month you are 65 or older and enrolled in Medicare Part B. During this specific time, federal law grants you Guaranteed Issue Rights, which means insurance companies cannot deny you a policy or charge you more because of your health history. This is the most vital phase of your medicare supplement open enrollment because it eliminates the barriers that often block seniors with chronic conditions from obtaining affordable supplemental coverage.

Understanding medical underwriting in Florida

Medical underwriting is the process insurers use to price risk based on health history. Once your initial window closes, Florida carriers typically require you to answer a 15 to 20 question health survey. They will ask about your history with insulin-dependent diabetes, heart stents, or any hospitalizations within the last 24 months. If you have these conditions, you risk being “locked-in” to your current coverage for the rest of your life. You won’t have the flexibility to switch to a lower-priced carrier if your health changes later, making that first choice in Florida incredibly impactful.

This same underwriting process can make securing other forms of financial protection, like life insurance, feel impossible for those with medical histories. Fortunately, specialized help is available. For individuals who have been declined for life insurance due to pre-existing conditions, services like Special Risk Term focus on finding affordable options.

The cost of missing your deadline

Waiting to apply can be an expensive mistake for Martin County residents. Most Florida carriers use “attained age” pricing, where premiums naturally increase as you get older. If you miss your window and apply later with a health condition, a carrier might add a 25 percent surcharge to your monthly bill or deny your application entirely.

Consider the case of a Jensen Beach senior who waited until age 70 to apply for Plan G. Because of a minor heart murmur diagnosed at age 68, they were denied coverage by three major Florida carriers and were forced to stay with their original, more expensive plan. You can avoid this by acting when your rights are protected. Benefits of applying during your window include:

- No waiting periods: Insurers cannot make you wait for coverage of pre-existing conditions like heart disease.

- Full plan access: You can choose any lettered plan (A through N) available in your Florida zip code.

- Price protection: Your premium is based on your age, not your medical records.

It’s helpful to compare medicare supplement plans with a local expert who understands the Florida market. Taking this step during your medicare supplement open enrollment ensures that you secure the lowest possible rate regardless of your health status. Our licensed agents provide a no-obligation review to help you understand how these federal protections apply to your specific situation in Martin County.

Florida-Specific Medigap Rules for Jensen Beach Residents

Florida manages Medigap plans through the Department of Financial Services. This state-level oversight ensures that your medicare supplement open enrollment period follows strict consumer protection guidelines. Unlike many other states, Florida mandates that insurance companies offer at least one Medigap policy to Medicare beneficiaries under age 65 who qualify because of a disability. This specific protection lasts for six months starting from the day you enroll in Medicare Part B. You can find deep-dive details in Florida’s official guidance on Medigap, which outlines how these state-specific mandates apply to your coverage.

In Martin County, the carrier landscape is dominated by established names like Florida Blue, Humana, and UnitedHealthcare. These companies offer various plans, but their network stability and local reputation vary. It’s also vital to address the “Birthday Rule” myth. While states like California or Oregon allow residents to switch plans around their birthday without medical underwriting, Florida doesn’t have this rule. Once your initial medicare supplement open enrollment window closes, you’ll likely face health questions and medical underwriting if you try to change plans later. This makes your first choice critical for your long-term financial health.

Working with a local Jensen Beach agent

Choosing a plan requires more than looking at a price tag. You need local expertise to ensure your coverage aligns with Treasure Coast healthcare systems. National call centers often don’t realize how specific plans interact with facilities like Cleveland Clinic Martin North. A local broker understands the 2026 Florida rate increases, which are projected to average between 4% and 8% for several major carriers. They help you compare these shifts across multiple independent providers to keep your monthly costs predictable.

Florida Medigap pricing structures

Florida allows three pricing models: community-rated, issue-age, and attained-age. Most plans available to Jensen Beach seniors use attained-age pricing. This means your premium is based on your current age and will increase as you get older. While these plans often start with the lowest monthly costs for 65-year-olds, they can become significantly more expensive by the time you reach your late 70s.

- Issue-age: Premiums are based on the age you are when you buy the policy and don’t increase due to aging.

- Attained-age: Premiums start low but increase annually as you grow older.

- Community-rated: Everyone in the same geographic area pays the same premium regardless of age.

To protect your fixed income, ask your agent to show you the historical rate stability of a carrier before you sign. Locking in a plan with a five-year track record of modest increases is the best way to ensure peace of mind in your 80s.

Comparing Popular Medigap Plans: Plan G vs. Plan N

Choosing the right coverage during your medicare supplement open enrollment period usually involves a choice between two primary options: Plan G and Plan N. Since January 1, 2020, federal law has prohibited new Medicare beneficiaries from purchasing Plans F or C. These older plans covered the Part B deductible, which is no longer allowed for those new to the system. Consequently, Plan G and Plan N have become the most reliable choices for Florida residents seeking to fill the gaps left by Original Medicare.

Plan G: Maximum peace of mind

Plan G is the “Gold Standard” for comprehensive coverage in 2026. It covers every gap in Medicare Part A and Part B except for the annual Part B deductible. In 2025, this deductible was $257, and you should expect a similar figure for 2026. A vital benefit for seniors on the Treasure Coast is the coverage of Part B excess charges. If a specialist in Stuart or Jensen Beach does not accept “Medicare assignment,” they can legally charge up to 15% more than the Medicare-approved rate. Plan G pays this entire amount for you. Plan G remains the most popular choice for Florida seniors seeking to eliminate nearly all out-of-pocket medical expenses.

Plan N: The budget-friendly alternative

Plan N offers lower monthly premiums than Plan G, which appeals to many retirees managing a fixed budget. In exchange for lower premiums, you agree to pay small co-pays for certain services. You will pay up to $20 for every office visit and up to $50 for emergency room visits that don’t lead to an inpatient admission. Like Plan G, you must meet the Part B deductible before the plan starts paying. However, Plan N does not cover Part B excess charges. This plan is often the best choice for Treasure Coast residents who see their doctors less frequently and want to reduce their fixed monthly insurance costs.

Your decision depends largely on your health needs and how you prefer to manage your finances. You can compare Medicare Supplement plans to see exactly how these premium differences look in your specific zip code. If you value a predictable monthly budget without any surprises at the doctor’s office, Plan G is the logical choice. If you’re healthy and don’t mind paying a small fee when you seek care, Plan N can save you hundreds of dollars in annual premiums.

Timing is everything during medicare supplement open enrollment. This window is your one-time opportunity to secure these plans without answering a single health question. Whether you choose the robust protection of Plan G or the cost-effective structure of Plan N, locking in your rate early ensures long-term security. For those considering all their options, it’s also worth exploring advantage plans medicare for 2026 to understand how network-based coverage compares to the freedom of Medigap plans.

Steps to Enroll: Your 2026 Florida Medigap Checklist

Securing a plan during your medicare supplement open enrollment window is the most effective way to guarantee coverage without medical underwriting. In Florida, this six-month window begins the first day of the month you are both 65 or older and enrolled in Medicare Part B. Missing this window can lead to higher monthly costs or a total denial of coverage later. Follow these four steps to ensure a smooth transition into your 2026 plan:

- Verify your Part B effective date: Look at the lower right corner of your red, white, and blue Medicare card. If you haven’t received your card yet, log into your Social Security account to confirm your status.

- Research local zip code rates: Medigap pricing is highly localized. A plan available in zip code 34957 may have a different premium than the same plan in a neighboring county.

- Compare carrier networks: Consult with a licensed agent to review the latest 2026 rates from Florida Blue, Aetna, and UnitedHealthcare (UHC). These companies use different pricing models that affect your long-term costs.

- Submit your application early: You don’t have to wait for your Part B to start. You can submit your application up to 6 months before your Part B effective date to lock in your spot.

When to start the process

The most successful enrollments begin at least 90 days before your birth month. This “3 months before” rule is essential for those turning 65 because it allows enough time to gather your Medicare ID number and current insurance records. If you’re currently covered by an employer, apply for your Medigap policy before that group coverage ends. This timing prevents a gap in protection and ensures you aren’t stuck paying the 20 percent coinsurance that Original Medicare doesn’t cover.

Finalizing your coverage

Once your policy is issued, Florida law provides a 30-day “Free Look” period. This allows you to review the policy details and return it for a full refund if the plan doesn’t meet your specific health needs. It’s a vital safety net for your peace of mind. To prevent a policy lapse, set up automatic premium payments through your bank. A single missed payment can put your coverage at risk, especially if you no longer have guaranteed issue rights. For a no-obligation review of your 2026 options, contact Florida Medicare Advantage today. Our local experts will help you compare the medicare supplement open enrollment choices available in your community.

Secure Your 2026 Florida Medigap Protection Today

Timing is everything for your medicare supplement open enrollment period. This 6-month window is your guaranteed opportunity to enroll in a plan without medical underwriting, meaning you can’t be charged more for your health history. Jensen Beach residents have unique options to weigh, such as the full coverage of Plan G versus the cost-effective structure of Plan N. Our Jensen Beach local office simplifies this process by putting you in touch with licensed Florida agents who live and work in your community. Because we operate as an independent brokerage, we provide unbiased comparisons of 2026 rates from Humana, UnitedHealthcare, and Florida Blue. You don’t need to spend hours deciphering federal handbooks when local expertise is readily available. Speak with a Jensen Beach Medicare expert for a free Medigap quote to ensure your healthcare costs remain predictable. We’re ready to help you find the right plan so you can enjoy your Florida retirement with absolute peace of mind.

Frequently Asked Questions

Can I change my Medigap plan during the Annual Enrollment Period (AEP)?

No, the Annual Enrollment Period from October 15 to December 7 doesn’t apply to Medigap plans. You can apply to change your Medicare Supplement policy at any time of the year. However, if you’re outside your initial six-month window, Florida insurance companies will likely require medical underwriting. This means they’ll look at your health history and could charge higher premiums or deny coverage based on pre-existing conditions.

What happens if I miss my 6-month Medigap Open Enrollment window in Florida?

You lose your guaranteed issue rights if you miss your six-month medicare supplement open enrollment period. This window begins the first day of the month you’re 65 or older and enrolled in Medicare Part B. After this period, Florida insurers typically require you to answer health questions. If you have chronic conditions like diabetes or heart disease, you may face higher monthly costs or be denied a policy entirely.

Does Florida have a “Birthday Rule” for switching Medicare Supplement plans?

Florida doesn’t currently have a “Birthday Rule” that allows you to switch Medicare Supplement plans without medical underwriting. While states like California and Oregon offer this 30-day window, Florida residents must typically pass a health screening to change plans. You should review your coverage annually with a licensed agent to see if you still qualify for lower rates based on your current health status and age.

Is medical underwriting required for Medigap in Florida if I have a Medicare Advantage plan?

Yes, medical underwriting is usually required if you want to switch from a Medicare Advantage plan to a Medigap policy in Florida. Unless you’re in a Trial Right period, such as your first 12 months on Medicare Advantage, insurers will evaluate your medical history. They use this data to determine your eligibility and premium costs. Always confirm your specific health status with a local expert before canceling your existing Advantage plan.

Can an insurance company deny me a Medigap policy during my open enrollment period?

No, an insurance company cannot deny you a policy or charge you more during your initial six-month medicare supplement open enrollment. Federal law mandates that insurers must sell you any Medigap policy they offer at the best available rate, regardless of your health. This protection applies even if you have serious pre-existing conditions like cancer or COPD. It’s the most secure time for Florida seniors to lock in comprehensive supplemental coverage.

How much do Medicare Supplement plans cost in Jensen Beach, FL?

Medicare Supplement Plan G premiums for a 65-year-old non-smoker in Jensen Beach typically range from $165 to $230 per month. Prices vary based on the specific insurance carrier and the plan type you choose; for example, Plan N often costs between $120 and $160. These rates are subject to annual adjustments. Speaking with a local expert ensures you find the most competitive pricing for the 34957 zip code.

Do I need to renew my Medigap policy every year?

You don’t need to manually renew your Medigap policy each year because these plans are guaranteed renewable. As long as you pay your monthly premiums on time, the insurance company cannot cancel your coverage. Your benefits remain the same year after year, even if you develop new health problems. However, it’s wise to request a no-obligation review annually to ensure your premium remains competitive within the Florida market.

Can I get a Medigap plan if I am under 65 and on Medicare in Florida?

Yes, Florida law requires insurance companies to offer Medicare Supplement policies to individuals under age 65 who qualify for Medicare due to disability. While federal law doesn’t mandate this, Florida Statute 627.6741 ensures you have access to at least one Medigap plan, typically Plan A. Be aware that premiums for those under 65 can be significantly higher, often exceeding $400 per month, until you reach your 65th birthday.