What if your health insurance costs increased by 10% every single year for the rest of your life just because you missed a single deadline? According to recent CMS data, seniors who fail to sign up during their Initial Enrollment Period face permanent late enrollment penalties that never go away. You’ve likely spent the last few months sorting through a mountain of national mailers and ignoring high-pressure calls from out-of-state centers. It’s confusing to track exactly when the door finally closes on your chance for Medicare 3 months after 65.

This guide will show you how to navigate these final months to ensure your coverage begins exactly when you need it without financial surcharges. You’ll learn the specific steps to avoid the Part B penalty and how working with local licensed agents in Jensen Beach can provide a no-obligation review. We will break down the timeline for your final enrollment window and explain how to secure the most comprehensive Florida coverage available today. By the end of this article, you’ll have the clarity needed to make an informed decision for your long-term health.

Key Takeaways

- Learn how to maximize the final stages of your 7-month Initial Enrollment Period to avoid costly, lifelong late-enrollment penalties.

- Understand how your effective date is determined when enrolling in medicare 3 months after 65, ensuring your Florida coverage begins without a gap.

- Compare the distinct advantages of Florida Medicare Advantage and Medigap plans to find the right fit for your Treasure Coast lifestyle.

- Follow a streamlined 5-step checklist designed to simplify your transition and secure your health benefits before your enrollment window closes.

- Discover how partnering with a local Jensen Beach agency provides the clarity and personalized guidance needed for long-term health security.

What is the Medicare Window 3 Months After 65?

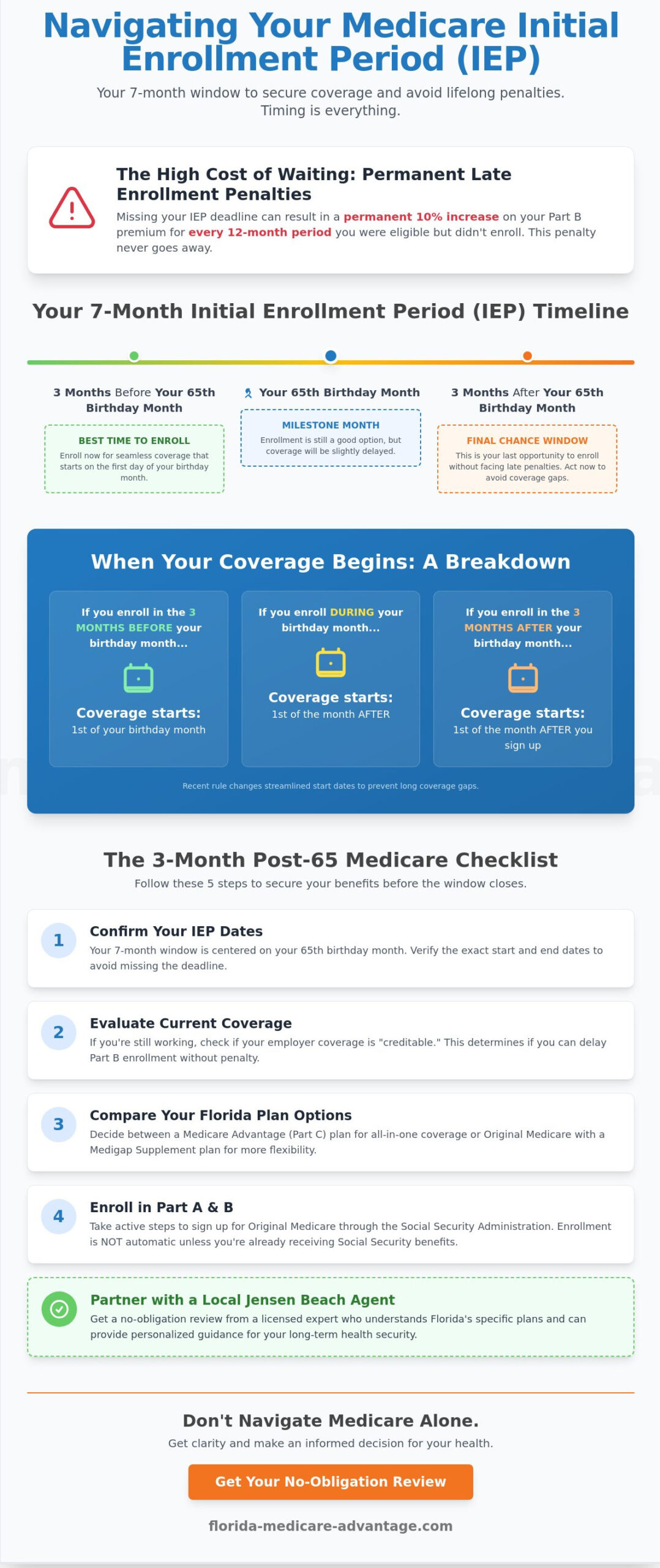

Entering your 65th birthday month is a major milestone for your health and your finances. For most residents in the Sunshine State, this period marks your first opportunity to join the Medicare program. This federal initiative provides the foundation for your healthcare coverage, but the rules regarding when to sign up are strict. You have a specific 7-month window called the Initial Enrollment Period (IEP) to make your choices without facing long-term financial consequences.

To better understand the nuances of timing your enrollment, watch this helpful video:

The 7-Month IEP Breakdown

Your enrollment timeline is anchored to your 65th birth month. It’s not a single deadline, but a sequence of months that dictate when your benefits actually begin. The 7-month window includes:

- The 3 months before your 65th birthday month

- The month of your 65th birthday

- The 3 months following your 65th birthday

Timing is everything. If you enroll during the first three months, your coverage typically starts the first day of your birth month. If you wait for the period of medicare 3 months after 65, your effective date is delayed. While you’re still within your rights to sign up, your coverage won’t begin until the first of the following month. This gap can leave you temporarily uninsured if you’ve already retired or lost employer-sponsored plans.

Why Florida Seniors Often Wait

In Martin County and across South Florida, many seniors hesitate to enroll exactly at 65. A common misconception is that enrollment happens automatically. This is only true if you’re already receiving Social Security benefits. If you aren’t, you must take active steps to sign up. Another reason for delay is continuing to work. If you have “creditable” coverage through a large employer with 20 or more employees, you might choose to defer Part B.

The window for medicare 3 months after 65 serves as your final safety net. It’s your “last call” to secure Part A and Part B without a permanent late enrollment penalty. This penalty adds 10% to your Part B premium for every full 12-month period you were eligible but didn’t sign up. Our licensed agents provide a no-obligation review to help you avoid these lifetime costs. We focus on local expertise to ensure you don’t feel overwhelmed by federal regulations. Speaking with a local expert helps bridge the gap between complex laws and your personal peace of mind.

Coverage Start Dates: When Does Medicare Begin if You Wait?

Timing your enrollment correctly ensures you don’t face a lapse in medical care or unexpected out-of-pocket costs. While your Initial Enrollment Period (IEP) lasts seven months, the date your benefits actually begin depends entirely on when you submit your application. If you wait until the final months of your window, you may find yourself without coverage during a critical transition period. This uncertainty can be stressful for those living on a fixed income who need to budget for healthcare expenses.

The Effective Date Timeline

The 2023 rule changes streamlined how the effective date is determined for those who delay. If you sign up during your 65th birthday month, your coverage begins on the first day of the following month. For those researching medicare 3 months after 65, the rules for the final three months of the IEP are now more predictable than in previous years. In 2026, Medicare coverage begins the first day of the month after you sign up if you enroll during the last three months of your IEP.

Following the Social Security Administration guidelines, the “First of the Month” rule applies to Florida Medicare Part B. This means your benefits will always start on the 1st, regardless of whether you applied on the 2nd or the 28th of the prior month. Here is how the timeline breaks down for late enrollees:

- Month 4 (Birthday Month): Coverage starts the 1st of Month 5.

- Month 5: Coverage starts the 1st of Month 6.

- Month 6: Coverage starts the 1st of Month 7.

- Month 7: Coverage starts the 1st of Month 8.

Avoiding the “Gap” in Jensen Beach

Waiting until the 7th month of your IEP is a high-risk strategy that often leads to a coverage gap. If your private insurance or COBRA ends on your 65th birthday, but you delay your application until the end of your window, you could spend 90 days or more without a safety net. This leaves you responsible for 100% of your medical bills during that time. Residents in Jensen Beach often need to coordinate the termination of their current plan with the exact start date of their new Florida Medicare plan to avoid these pitfalls. Even a short 30-day gap can result in thousands of dollars in hospital fees if an emergency occurs.

Our licensed agents frequently see seniors struggle with the overlap between employer group plans and Part B. To ensure a seamless transition without a single day of exposure, you should review your turning 65 Medicare options at least 120 days before your birthday. Proactive planning helps you secure the peace of mind that comes with continuous, reliable health coverage. Understanding the nuances of medicare 3 months after 65 is essential for anyone who missed their initial three-month window before their birthday.

Choosing Your Path: Florida Medicare Advantage vs. Supplement Plans

Deciding between a Medicare Advantage plan and a Medigap policy is the most critical step in your enrollment journey. This choice dictates how you access doctors in the Treasure Coast and what your out-of-pocket expenses look like. While your Initial Enrollment Period begins early, it actually extends to include medicare 3 months after 65. This timeframe allows you to evaluate how each path aligns with your specific health needs and budget.

The decision you make today carries long-term weight. If you miss certain windows, you might face medical underwriting later, which can make changing plans more difficult or expensive. Understanding your turning 65 Medicare options ensures you don’t lose access to the coverage styles you prefer as you age. Our licensed agents often see residents feel rushed, but taking a methodical approach now provides security for years to come.

Medicare Advantage in Florida

Medicare Advantage, or Part C, replaces Original Medicare with coverage managed by private insurers. In Martin County, residents have access to robust networks from various reputable providers. These plans are popular because they often include “extra” benefits that Original Medicare doesn’t cover. You can find many Medicare Advantage plans that bundle the following services:

- Comprehensive dental exams, cleanings, and X-rays.

- Vision care, including annual exams and allowances for frames or contacts.

- Hearing aid fittings and hardware discounts.

- Fitness memberships through programs like SilverSneakers.

These plans generally have lower monthly premiums, sometimes as low as $0. However, you must use the plan’s network of doctors to keep costs low. It’s a “pay-as-you-go” model where you pay co-pays when you visit a specialist or facility.

Medicare Supplement (Medigap) Considerations

Medicare Supplement plans work alongside Original Medicare to pay for costs like deductibles and the 20 percent coinsurance that Part B doesn’t cover. The biggest advantage here is the “guaranteed issue” right. During your first 6 months of having Part B, insurance companies can’t deny you coverage or charge more for pre-existing conditions. This is why it’s vital to compare Medicare Supplement plans while you are in your initial window.

Medigap offers predictable monthly costs. You pay a higher premium than Advantage plans, but your out-of-pocket costs at the doctor’s office are often zero or very low. There are no networks; you can see any doctor in the United States who accepts Medicare. This flexibility is a top priority for Florida retirees who travel frequently or have specific specialists in mind. Remember that your window to join without a health screening ends shortly after you turn 65, making the timing of your application essential for your financial protection.

The 3-Month Post-65 Medicare Checklist: 5 Steps to Take Now

The window for your Initial Enrollment Period is closing. If you’re currently in the phase of medicare 3 months after 65, you’ve entered the final stage of your seven-month enrollment window. Missing these deadlines can result in lifelong late enrollment penalties and delayed coverage for essential medical services here in Florida. Follow these steps to secure your health benefits without the stress of last-minute filing.

Step 1: Verify Your Part A and Part B Status

Check your mail for your red, white, and blue Medicare card. If you’ve received Social Security benefits for at least four months before your 65th birthday, the government usually enrolls you automatically. If you don’t see a card, visit SSA.gov immediately to create an account and apply. You must actively sign up for Part B if you are not yet receiving Social Security benefits by age 65. Failing to do so can leave you without outpatient coverage when you need it most. Review the full timeline of Medicare enrollment periods to ensure you aren’t missing a critical cutoff.

Step 2: Evaluate Your Prescription Drug Needs

Medicare Part D isn’t optional if you want to avoid future costs. If you go 63 days or more without creditable drug coverage, you’ll face a permanent late enrollment penalty. This penalty adds 1% of the national base beneficiary premium to your monthly cost for every month you were eligible but didn’t join. When comparing Medicare Part D plans, check the specific formularies for your medications. Ensure your preferred Jensen Beach pharmacies, such as the Publix on Northeast Jensen Beach Boulevard or local Walgreens, are in-network to keep your out-of-pocket costs low.

Step 3: Consult a Local Florida Agent

National call centers often rely on generic scripts and don’t understand the Treasure Coast healthcare landscape. A local expert knows which plans are accepted by Cleveland Clinic Martin Health and which doctors in Jensen Beach are currently taking new patients. Working with a local professional helps you avoid the high-pressure tactics found in generic television ads. We provide a no-obligation coverage review to help you find a plan that fits your budget and health needs. Our licensed agents prioritize your long-term stability over a quick transaction.

Step 4: Compare Advantage and Supplement Options

Decide between a Medicare Advantage plan or a Medigap policy. Advantage plans often include extra benefits like dental and vision, while Medigap helps pay for out-of-pocket costs like the 20% coinsurance under Part B. Your choice depends on your budget and how often you visit specialists in Stuart or Port St. Lucie.

Step 5: Schedule Your Welcome to Medicare Visit

Once your coverage is active, you’re eligible for a one-time “Welcome to Medicare” preventive visit. This must happen within the first 12 months of your Part B enrollment. It’s a great way to establish a baseline with a local Florida primary care physician and develop a long-term wellness plan.

Don’t let your enrollment window slip away. Speak with a local expert for a no-obligation review to secure your coverage today.

Secure Your Florida Coverage: Why Local Expertise Matters

Choosing a Medicare plan is one of the most significant financial decisions you’ll make this decade. While the federal government provides the framework, your healthcare experience is local. Your doctors, your pharmacy, and your neighborhood hospitals determine how your plan actually works for you. Transitioning from your Initial Enrollment Period (IEP) into long-term health security requires more than just picking a name from a brochure. It requires a strategy tailored to the Florida market. Working with a local expert ensures you don’t overlook the nuances of regional networks.

If you miss your initial window, you might face late enrollment penalties or gaps in coverage. However, certain life events allow for a special enrollment period for Medicare. These periods are vital for seniors who move to a new area or lose employer coverage. Understanding how to use medicare 3 months after 65 to your advantage is critical. This period marks the final stage of your IEP. Once it closes, your options may become more limited until the next annual enrollment cycle. The window for medicare 3 months after 65 is your final opportunity to secure coverage that begins without a lengthy delay.

The Jensen Beach Advantage

Working with a local agency provides a level of accountability that national call centers can’t match. Our licensed agents are available for face-to-face consultations at 1041 NE Jensen Beach Blvd. We understand the Martin County healthcare network intimately. We know which plans are accepted at Cleveland Clinic Martin North and which ones offer the best networks for specialists in Stuart or Port St. Lucie. This local knowledge ensures your coverage isn’t just a policy, but a functional tool for your health. Our support doesn’t end when you sign the paperwork. We remain your point of contact as your health needs change over the years.

Your Next Steps

Before your 7th month of eligibility expires, you should finalize your plan comparison. Gather your list of current medications and your preferred provider names. Having these documents ready allows us to run an accurate cost analysis. This data-driven approach often reveals significant differences in out-of-pocket maximums between various Florida Medicare Advantage plans. You don’t have to guess which option is best. Visit the Florida Medicare Advantage home page to start your research or schedule a no-obligation review. Taking action now secures your peace of mind for the future. Let’s ensure your 65th year is the start of a healthy, well-protected retirement.

Take Control of Your Medicare Enrollment Today

Navigating the final days of your Initial Enrollment Period requires precision. The window for medicare 3 months after 65 represents your last chance to secure coverage without facing lifetime late enrollment penalties. Missing this federal deadline can increase your Part B premiums by 10% for every full 12-month period you were eligible but didn’t sign up. You’ve worked hard for these benefits; don’t let a simple calendar oversight jeopardize your financial security or your access to quality healthcare.

Deciding between Florida Medicare Advantage and a Supplement plan is a personal choice that impacts your long-term health outcomes. Our licensed Florida insurance agency operates a local Jensen Beach office, not a distant call center. We provide the clarity you need by representing top-rated carriers. We’ll help you review the 5-step checklist to ensure your coverage starts exactly when you need it. You deserve a plan that accounts for your specific doctors and local provider networks.

Stop worrying about complex federal regulations and start feeling confident in your choices. Speak with a Local Jensen Beach Medicare Expert Today for a no-obligation review of your options. We’re here to help you transition into this new chapter with total peace of mind.

Frequently Asked Questions

Can I still sign up for Medicare if I am 3 months past my 65th birthday?

Yes, you can still enroll because your Initial Enrollment Period lasts for a full 7 months. This window includes the 3 months before you turn 65, your birth month, and the 3 months following it. If you are seeking coverage medicare 3 months after 65, you are currently in the final month of your guaranteed enrollment window. Acting now ensures you secure your benefits before this specific period expires.

What happens if I miss the 7-month Initial Enrollment Period in Florida?

If you miss this window, you must wait until the General Enrollment Period to sign up. This period occurs annually from January 1 through March 31. Your coverage won’t begin until the first of the month after you enroll. You may also face a lifetime late enrollment penalty of 10 percent for every 12 month period you were eligible for Part B but didn’t have it.

Will I face a late enrollment penalty if I sign up 3 months after turning 65?

You won’t face any late enrollment penalties if you sign up during this time. Since the 7 month Initial Enrollment Period includes the 3 months after your 65th birthday, you’re still within the federal timeline. It’s a safe time to finalize your medicare 3 months after 65 plans. Submitting your application before this window closes protects you from the permanent Part B premium increases that affect late enrollees.

When will my Medicare coverage start if I enroll in the last month of my IEP?

Your Medicare coverage will start on the first day of the month after you complete your enrollment. If you wait until the seventh month of your Initial Enrollment Period, there’s a slight delay compared to those who joined early. For instance, an enrollment submitted in the final days of your window results in benefits starting the following month. This timing is vital for Florida seniors to understand to avoid a gap in care.

Do I need to sign up for Medicare if I am still working in Florida at 65?

Your need to enroll depends on the size of your employer. If your company has 20 or more employees, you can usually delay Part B without a penalty because your group coverage is primary. If your Florida employer has fewer than 20 employees, Medicare typically becomes your primary insurance at age 65. You should check with your benefits coordinator to confirm how your specific plan coordinates with federal requirements.

What is the difference between the Initial Enrollment Period and the General Enrollment Period?

The Initial Enrollment Period is a one time 7 month window for people new to Medicare. It offers the most flexibility and carries no risk of late fees. The General Enrollment Period is a yearly backup for those who missed their first chance. It runs from January 1 to March 31 each year. Using the General Enrollment Period often results in higher monthly premiums and a delay in when your health coverage actually starts.

How do I find the best Medicare Advantage plan in Jensen Beach?

Finding the right plan in Jensen Beach requires a review of the specific provider networks in Martin County. Plans are localized by zip code, so options in 34957 may differ from those in nearby cities. You should compare the 2024 drug formularies and out of pocket maximums for every available carrier. A local expert can provide a side by side comparison of plans that include your specific doctors and preferred local pharmacies.

Is there a cost to work with a Medicare agent at Florida Medicare Advantage?

There’s no cost to you for a consultation or a no-obligation review with our team. Our licensed agents are compensated by the insurance carriers, which means you receive professional guidance at zero charge. You get access to local expertise and plan comparisons without any hidden fees or added premiums. This service is designed to give you peace of mind while ensuring you find a plan that fits your budget and health needs.