What if a single oversight this year led to a permanent 10% increase in your monthly premiums for the rest of your life? For many Florida seniors, missing the medicare deadline for enrollment isn’t just a minor inconvenience; it’s a costly mistake that impacts a fixed income indefinitely. You likely feel overwhelmed by the constant stream of national robocalls and the confusing alphabet soup of IEP, AEP, and GEP. It’s completely natural to feel frustrated when all you want is clear, local guidance from someone who understands our state’s unique market.

You deserve to move into 2026 with total confidence in your healthcare choices. This guide provides a clear roadmap of the critical dates you need to know, including the October 15 start of the Annual Enrollment Period. We’ll help you identify if you qualify for a Special Enrollment Period and show you how to secure your coverage without the stress. You’ll master the 2026 timeline with the help of a local expert who prioritizes your long-term health outcomes over a quick sale.

Key Takeaways

- Master the 7-month window surrounding your 65th birthday to ensure your 2026 Florida coverage begins without delay.

- Protect your retirement savings by understanding how to avoid the permanent lifetime penalties associated with missing the medicare deadline for enrollment.

- Identify the specific life events, such as moving to Florida or losing employer coverage, that trigger a Special Enrollment Period for your benefits.

- Learn why a no-obligation review with a local licensed agent is the most efficient way to compare plans from multiple leading carriers.

Table of Contents

- Understanding the Medicare Enrollment Deadlines in Florida for 2026

- The Initial Enrollment Period (IEP): Your First 7-Month Window

- Late Enrollment Penalties: The Cost of Missing the Deadline

- Special Enrollment Periods (SEP): Florida-Specific Exceptions

- How a Local Florida Agent Simplifies the 2026 Enrollment Process

Understanding the Medicare Enrollment Deadlines in Florida for 2026

A medicare deadline for enrollment is a legally mandated window that determines when you can secure health coverage without facing lifetime financial penalties. These dates are strict. The federal government rarely grants exceptions for missed windows, making it vital for Florida residents to track their specific eligibility dates. For a comprehensive Medicare program overview, it is helpful to remember that the system relies on these windows to manage risk and ensure stable premiums for everyone in the pool.

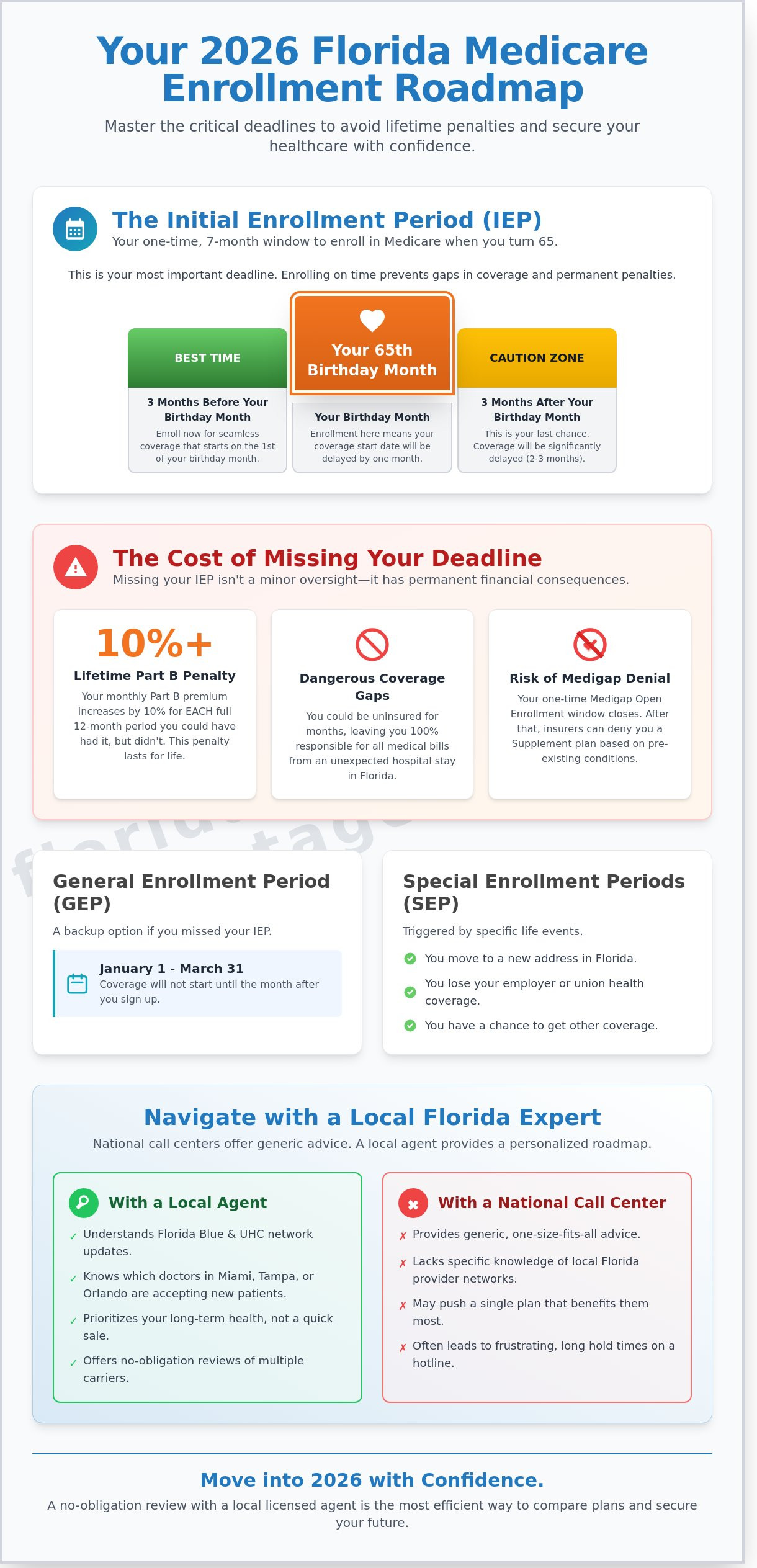

If you turn 65 in 2026, your primary medicare deadline for enrollment is your Initial Enrollment Period. This is a seven-month window. It begins three months before your 65th birthday month, includes your birth month, and extends for three months after. For example, if your birthday is June 15, 2026, your window opens March 1 and closes September 30. Missing this specific timeframe can delay your coverage and trigger the Part D late enrollment penalty, which adds a permanent cost to your monthly premium.

Beyond the initial window, Florida seniors should be aware of two other periods:

- General Enrollment Period: This runs from January 1 to March 31 each year for those who missed their initial window. Coverage won’t start until the month after you sign up.

- Special Enrollment Periods (SEP): These are triggered by specific life events, such as moving to a new zip code in Florida or losing employer-based coverage.

The Consequences of Missing Your Window

Missing your enrollment window creates immediate gaps in medical coverage. This often leads to high out-of-pocket costs at Florida hospitals if an emergency occurs while you’re uninsured. You may also face difficulty passing medical underwriting for Medigap plans. In Florida, your best opportunity to compare Medicare Supplement plans without health questions is during your initial six-month Medigap Open Enrollment Period. Once that window shuts, private insurers can deny coverage based on pre-existing conditions. The emotional stress of navigating these federal rules without local guidance can be overwhelming for many seniors.

Why a Local Florida Perspective Matters

National deadlines don’t account for the unique landscape of Florida healthcare. Local agents understand the timing for Florida Blue and UnitedHealthcare network updates which often occur late in the calendar year. While a national call center might provide generic advice, a local expert knows which doctors in Miami, Tampa, or Orlando are currently accepting new patients. We prioritize long-term health outcomes over quick transactions. Our turning 65 Medicare options review provides a personalized roadmap. You get the clarity of local expertise instead of the frustration of a generic government hotline.

The Initial Enrollment Period (IEP): Your First 7-Month Window

The Initial Enrollment Period (IEP) stands as the most critical medicare deadline for enrollment for most Floridians. This seven month window is built around your 65th birthday. It includes the three months before your birth month, the month you turn 65, and the three months following that date. Missing this specific window often leads to lifetime late enrollment penalties for Part D, which are added to your monthly premium for as long as you have coverage.

Florida residents should pay close attention to the “First of the Month” rule. If you enroll during the first three months of your IEP, your 2026 coverage begins on the first day of your birth month. For example, if your birthday is July 15, your coverage starts July 1. However, there’s a unique exception for those born on the first day of any month. If your birthday is October 1, Medicare actually treats you as if you turned 65 in September. In this case, your benefits begin on September 1, and your enrollment window shifts one month earlier.

Signing up during the initial three months is the only guaranteed way to prevent a lapse in your medical and prescription drug coverage. If you wait until your birthday month or the three months after, your start date is pushed back. This delay can leave you responsible for 100 percent of your healthcare costs during those gap months. For 2026 coverage, proactive planning is the best strategy to protect your retirement savings and ensure continuous access to your doctors.

Turning 65 in Florida: A Step-by-Step Timeline

In months one through three, focus on gathering your Social Security documents and researching local options. This is the ideal time for comparing Florida Medicare Advantage plans to see which networks include your preferred specialists in cities like Tampa or Orlando. During month four, your birthday month, you should be finalizing your application. If you wait until months five through seven, you enter the “Safety Net” period. While you can still enroll, your coverage won’t start until the first of the following month, which creates a risky period without insurance protection.

Working Past 65 in the Sunshine State

Many Floridians continue working well past age 65 and maintain employer health benefits. You must verify if your employer group health plan counts as “creditable coverage” by Medicare standards. If your Florida employer has fewer than 20 employees, Medicare usually becomes the primary payer at age 65. In this situation, you must enroll in Part B immediately to avoid massive out-of-pocket bills. When you eventually decide to retire, you can transition from group insurance to Medicare Advantage plans through a Special Enrollment Period. The process of signing up for Medicare Part B is managed by the Social Security Administration, and our local agents can help you time this transition to avoid any overlap or gaps.

Understanding these specific dates ensures you don’t pay more than necessary for your healthcare. If you’re unsure where you fall in this timeline, you can speak with a local expert for a no-obligation review of your enrollment status.

Late Enrollment Penalties: The Cost of Missing the Deadline

Missing the medicare deadline for enrollment triggers financial consequences that never expire. These surcharges aren’t one-time fines; they are permanent additions to your monthly costs. Medicare Part B carries a permanent 10% penalty for every full 12-month period you were eligible but delayed enrollment. If you wait 36 months to sign up, your Part B premium stays 30% higher for as long as you have the coverage. This can add hundreds of dollars to your annual healthcare spending over time.

The Part D penalty follows a different calculation but remains just as persistent. Medicare calculates this surcharge by taking 1% of the national base beneficiary premium for every full month you went without creditable coverage. For those looking ahead, these costs are tied to the 2026 national base beneficiary premium, which serves as the benchmark for your monthly surcharge. Because the base premium often changes annually, your penalty amount can actually increase every year. Our licensed agents often see Florida seniors surprised by how quickly these small percentages grow into significant monthly burdens.

Avoiding the Part D Late Enrollment Penalty

You can avoid this lifetime surcharge by maintaining what Medicare calls creditable prescription drug coverage. In Florida, this means your current insurance must be expected to pay at least as much as Medicare’s standard prescription drug coverage. You might feel tempted to skip a Medicare Part D plan if you don’t currently take any medications. This is a common mistake that leads to penalties later. Choosing a low-cost plan early protects your future budget. Many Florida Medicare Advantage plans bundle drug coverage directly into their benefits. This simplifies your experience and ensures you meet the medicare deadline for enrollment without managing multiple policies.

The General Enrollment Period (GEP) Fallback

If you miss your initial window, you must wait for the General Enrollment Period to sign up. This window opens every year from January 1 through March 31. You can review the Social Security Administration’s Medicare enrollment deadlines to confirm exactly when you can submit your application. Relying on the GEP is risky because your coverage doesn’t start until the month after you sign up. This creates a dangerous gap in your medical protection. During the GEP application process, Medicare will automatically assess any mandatory penalties based on how many months you delayed. We recommend a no-obligation review of your timeline to ensure you don’t end up paying more than necessary for your Florida healthcare coverage.

Special Enrollment Periods (SEP): Florida-Specific Exceptions

Life changes often happen outside the standard calendar. If you miss a typical medicare deadline for enrollment, you might still avoid the Part D penalty through a Special Enrollment Period (SEP). These windows allow you to join or switch plans without the usual restrictions. In Florida, these exceptions are vital for maintaining continuous coverage as your health needs or living situations evolve.

Relocating to the Sunshine State is a primary trigger for an SEP. You generally have a 2-month window starting from the month you move to secure a plan that serves your new Florida zip code. Similarly, if you’re leaving employer-sponsored coverage, you must act quickly. While you have 8 months to sign up for Part B, the window for Part D is only 63 days. Missing this shorter window often leads to a lifetime penalty. Florida residents qualifying for Medicaid or the “Extra Help” program gain even more flexibility. These individuals can change their drug coverage once per calendar quarter during the first nine months of the year.

- Moving to Florida: A 60-day window to align your coverage with local providers after establishing residency.

- Losing Employer Insurance: A 2-month limit to pick up Part D after your group coverage ends to avoid surcharges.

- Extra Help and Medicaid: Quarterly enrollment opportunities for those who meet specific income and asset thresholds.

- Chronic Conditions: Special Needs Plans (C-SNPs) for residents with diabetes or chronic heart failure often allow for mid-year enrollment.

Hurricane and Disaster-Related SEPs

Florida’s weather is unpredictable, and the official hurricane season runs from June 1 through November 30. When FEMA declares a disaster area, Medicare often grants an emergency enrollment window. This extension helps residents who couldn’t meet a medicare deadline for enrollment because of a storm, power outage, or evacuation. If a major weather event prevents you from submitting your application, you may qualify for additional time. Our local agents monitor Florida Division of Emergency Management updates to help neighbors claim these extensions when they occur.

Moving into a Florida Long-Term Care Facility

Transitioning into an assisted living facility or skilled nursing home is a major life event. This move triggers a specific SEP that lasts as long as you live in the facility and for two months after you leave. It’s an ideal time to evaluate if your current drug plan meets your new medical requirements. If you’re new to Medicare and entering a facility, specialized plans may offer better coordination of care. This window ensures your medications remain affordable during a sensitive transition.

Don’t let a missed deadline cost you money for years to come. Contact a local expert for a no-obligation review of your Florida Medicare options today.

How a Local Florida Agent Simplifies the 2026 Enrollment Process

Missing the medicare deadline for enrollment leads to more than just a temporary headache. It results in a permanent monthly penalty that follows you for the rest of your life. A licensed Florida agent provides a no-obligation review to identify your specific Initial Enrollment Period based on your 65th birthday. This personalized roadmap ensures you don’t miss the seven-month window that begins three months before you turn 65. By working with a local expert, you replace the anxiety of federal timelines with a clear, actionable schedule.

Comparing top-rated carriers like Humana, Florida Blue, and UnitedHealthcare often feels overwhelming when done alone. Each carrier has different drug formularies and star ratings that impact your out-of-pocket costs. A local agent compares these options in one sitting, saving you from hours of repetitive phone calls to national centers. They verify that your preferred Florida doctors and local pharmacies are in-network before you commit to a plan. This step is vital because provider networks in the Sunshine State can change, and you need to know your specialist is covered before the medicare deadline for enrollment passes.

Your relationship with an agent continues long after you sign your initial paperwork. They provide ongoing support to manage plan changes during the Annual Enrollment Period (AEP) from October 15 to December 7 each year. If your medication costs rise or your primary care physician leaves a network, your agent is ready to help you pivot to a better option for the following year.

The Advantage of Independent Brokerage

Working with an independent agent offers significantly more choices than calling a single carrier directly. Captive agents only sell products from one company, but independent brokers represent multiple plans across the Florida market. This “client-first” mentality prioritizes your specific health needs over a quick sale. For residents in Jensen Beach and Martin County, local experts understand the nuances of regional networks, such as which plans offer the best access to Cleveland Clinic or local specialized clinics.

Your 2026 Medicare Readiness Checklist

- Confirm your Social Security status at least 120 days before your 65th birthday to ensure your Part A and Part B are active.

- Review the best Medicare Advantage plans available for your specific Florida zip code to see updated 2026 benefits.

- Schedule a consultation with a licensed Florida Medicare Advantage agent to verify your prescription drugs are on the plan’s formulary.

- Finalize your selection at least one month before your birthday to avoid any gap in medical or prescription coverage.

Choosing the right path requires local expertise and a steady hand. Speak with a local expert today to secure your coverage and gain the peace of mind that comes with professional guidance.

Take Control of Your 2026 Florida Healthcare Future

Navigating the complex world of federal benefits doesn’t have to be a source of stress. Missing your specific medicare deadline for enrollment can lead to permanent financial consequences. According to the Centers for Medicare & Medicaid Services (CMS), you face a 10% premium penalty for every full 12-month period you lacked Part B coverage. Your Initial Enrollment Period is a strict 7-month window that centers around your 65th birthday. Florida seniors also have unique access to Special Enrollment Periods during state-declared emergencies or when relocating between Florida counties. These local exceptions provide vital flexibility when your circumstances change unexpectedly.

Our licensed independent agents provide the local clarity you need for the 2026 coverage year. We offer no-obligation plan comparisons tailored to your specific zip code and health requirements. You don’t have to guess which network includes your doctors or which plan covers your prescriptions. We bring professional expertise directly to you to ensure you’re fully protected. Speak with a Licensed Florida Medicare Expert for a Free Deadline Review today. Your health is your most valuable asset; let’s work together to protect it for the years ahead.

Frequently Asked Questions

What is the absolute deadline to sign up for Medicare in 2026?

The absolute medicare deadline for enrollment for most seniors is the final day of their seven-month Initial Enrollment Period. If your 65th birthday is July 15, 2026, your window opens April 1 and closes October 31. Missing this specific timeframe can lead to permanent late enrollment penalties that increase your monthly premiums for the rest of your life.

Is there a penalty if I wait until I am 66 to sign up for Medicare in Florida?

You’ll likely face a lifelong financial penalty if you wait until age 66 to sign up without having creditable coverage from an employer. The Part B premium increases by 10% for each full 12-month period you were eligible but didn’t enroll. In Florida, our licensed agents help you calculate these costs to ensure you make an informed decision before your window closes.

Can I change my Medicare plan if I move to Florida from another state?

Moving to Florida from another state triggers a Special Enrollment Period that allows you to change your plan. This window typically lasts for two full months after the month you move to your new Florida residence. It’s a vital time to speak with a local expert because your previous state’s network won’t cover your healthcare needs in cities like Tampa or Orlando.

What happens if I missed the Medicare open enrollment period?

If you missed the fall Annual Enrollment Period, you can still make changes during the General Enrollment Period from January 1 to March 31 each year. Your new coverage will begin the first day of the month after you submit your application. This period is a second chance for Florida residents to secure the peace of mind that comes with proper healthcare coverage.

Do I have to sign up for Medicare every year?

You don’t need to re-enroll in Medicare every year because your coverage generally renews automatically. However, 100% of beneficiaries should review their plan during the Annual Election Period from October 15 to December 7. Plans often change their formularies or provider networks, so a no-obligation review with a local agent ensures your benefits remain competitive for the upcoming year.

What is the Medicare deadline for enrollment if I am still working at 65?

Your specific medicare deadline for enrollment is an eight-month Special Enrollment Period that begins the month after your group health coverage or employment ends. If your job ends on May 31, you have until January 31 of the following year to sign up without penalty. Florida seniors often find that transitioning to a Medicare Advantage plan provides more comprehensive benefits than their previous employer-sponsored insurance.

How do I avoid the Medicare Part D late enrollment penalty in Florida?

You avoid the Part D late enrollment penalty by maintaining creditable prescription drug coverage that’s expected to pay as much as standard Medicare. If you lose this coverage, you must join a Medicare drug plan within 63 days to stay penalty-free. Keep your Certificate of Creditable Coverage in a safe place so our licensed agents can verify your status and protect your savings.

Are there special Medicare deadlines for Florida hurricane victims?

Florida residents affected by FEMA-declared emergencies, such as 2024 hurricanes, often qualify for an extension to enroll in or switch plans. This Special Enrollment Period typically lasts for four full months after the disaster declaration date. If a storm disrupted your ability to meet a deadline, contact a local consultant to see if you qualify for this additional time to secure your benefits.