What if a single missed deadline in 2026 cost you thousands of dollars in cumulative penalties over the next two decades? It’s frustrating to manage complex acronyms like IEP and AEP while your phone rings constantly with robocalls from national call centers. You deserve the security of knowing your medications are covered without the threat of a permanent monthly surcharge. This guide simplifies the medicare pdp enrollment period for Florida seniors, ensuring you secure the right Part D plan while avoiding the common mistakes that lead to lifelong financial consequences.

We’ll provide a direct calendar of Florida enrollment dates and a clear explanation of how to sidestep the 1% monthly late enrollment penalty. You will learn how to distinguish between Initial, Annual, and Special enrollment windows with the help of a knowledgeable local expert. Our goal is to replace your anxiety with a simple roadmap to maintain continuous coverage through a licensed agent who understands the specific needs of our Sunshine State communities.

Key Takeaways

- Understand how missing the medicare pdp enrollment period can lead to lifelong financial penalties and learn how to avoid these common pitfalls.

- Identify the critical differences between your Initial Enrollment Period and the Annual Enrollment Period to ensure your drug coverage remains uninterrupted.

- Explore Florida-specific Special Enrollment Periods, including how local FEMA declarations and moving can grant you additional time to switch plans.

- Follow a clear, step-by-step guide to comparing formularies from major Florida carriers to find the most cost-effective prescription coverage.

- Learn why partnering with a local licensed expert offers a more personalized, no-cost alternative to impersonal national call centers.

Medicare PDP Enrollment Period: Why Timing is Critical for Florida Seniors

For the 4.9 million Medicare beneficiaries living in the Sunshine State, timing isn’t just a matter of convenience; it’s a matter of financial security. The medicare pdp enrollment period refers to the specific windows of time when you can join, switch, or drop a prescription drug plan. Because Medicare isn’t a static program, these dates dictate your access to affordable medications for the entire calendar year. Missing a deadline doesn’t just mean waiting; it often results in coverage gaps that leave you paying full retail price for prescriptions at your local pharmacy.

To help you visualize how these timelines work and why they matter, watch this clear breakdown of the process:

Florida seniors generally choose between two paths for drug coverage. You can select a standalone Medicare Part D plan to pair with Original Medicare, or you can receive benefits through a Florida Medicare Advantage plan that includes drug coverage. Florida’s high retiree population means our local market is competitive, with dozens of private insurers offering different formularies and price points. Understanding your medicare pdp enrollment period ensures you can navigate these options without facing a lapse in care.

What is a Prescription Drug Plan (PDP)?

A PDP is a standalone policy that adds drug coverage to Original Medicare. While Medicare Part D is a federal program, it’s administered by private insurance companies approved by Medicare. These companies decide which drugs they cover and what your co-pays will be. It’s wise to consider a plan even if you currently take zero medications. Enrolling early provides a safety net for unexpected health changes and protects you from future penalties. Our licensed agents often see residents who regret waiting until they receive a new diagnosis to look for coverage.

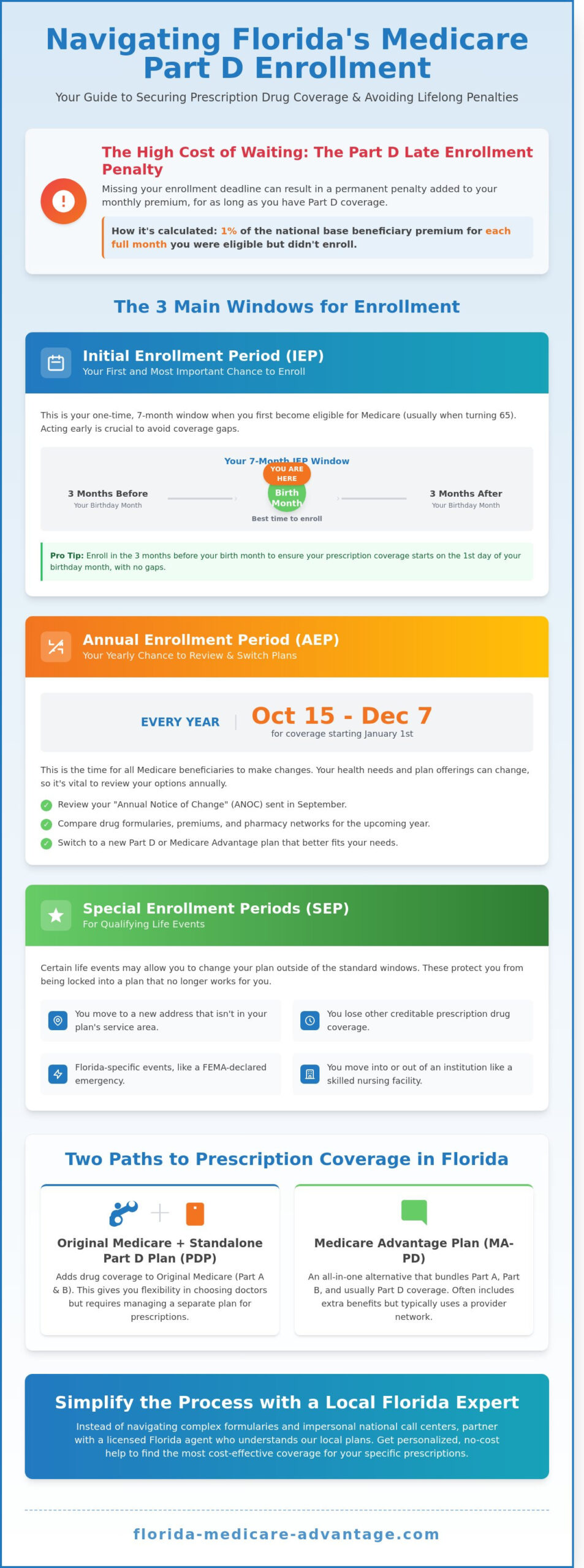

The Cost of Waiting: The Part D Late Enrollment Penalty

The Three Main Windows for Florida Medicare Part D Enrollment

Timing is everything for Florida residents seeking prescription drug coverage. Missing a deadline doesn’t just mean a delay in service; it can lead to lifelong financial penalties. For the 2026 plan year, you must track three primary windows to manage your medicare pdp enrollment period effectively. Understanding these dates ensures you maintain access to necessary medications without interruption.

Initial Enrollment Period (IEP) for Part D

Your Initial Enrollment Period is a unique seven-month window. It begins three months before the month you turn 65, includes your birth month, and extends for three months after. Enrolling during the first three months is the smartest move for Florida seniors. This ensures your coverage begins the first day of your birth month. If you wait until your birthday month or later, your start date will be delayed. You can explore your specific Turning 65 Medicare Options to see how this timeline fits your birthday. Acting early provides peace of mind and prevents the 1 percent per month late enrollment penalty.

Annual Enrollment Period (AEP): Oct 15 – Dec 7

The Annual Enrollment Period runs from October 15 through December 7 every year. This is the time for Jensen Beach residents to review their Annual Notice of Change (ANOC). Insurance companies send these letters in September. They detail changes to premiums, pharmacy networks, and drug formularies for 2026. Because Florida PDP options change annually, reviewing this document is vital. You can switch from one plan to another during this time without any medical underwriting. This guide to enrolling in Medicare Part D provides additional context on how these yearly changes affect your costs. If your current plan is raising prices, you can find more affordable medicare part d plans during this window.

Medicare Advantage Open Enrollment Period (MA-OEP)

The Medicare Advantage Open Enrollment Period occurs from January 1 to March 31. This window is specifically for Florida seniors already enrolled in a Medicare Advantage plan. If you find your current network doesn’t meet your needs in 2026, you can make a change. You have the right to switch to a different Advantage plan or return to Original Medicare. If you choose the latter, you are allowed to add a standalone Part D plan to maintain drug coverage. This is a crucial safety net for those who realize their current plan lacks the specific pharmacy access they require. Identifying the correct medicare pdp enrollment period for your situation prevents gaps in your medication history.

Our licensed agents offer a no-obligation review to help you track these dates. You can speak with a local expert to ensure you never miss a deadline and secure the most cost-effective coverage for your needs.

Florida-Specific Special Enrollment Periods (SEP)

Life changes frequently happen outside the standard fall window. When these events occur, you gain access to a Special Enrollment Period (SEP). This allows you to join or switch a Medicare Part D plan without waiting for the next October. For Florida seniors, these windows are critical for maintaining continuous prescription coverage while adapting to new circumstances.

Relocating to the Sunshine State

Moving your primary residence to Florida is one of the most common reasons to trigger a new medicare pdp enrollment period. Medicare drug plans are tied to specific service areas. If you move from another state, or even between certain Florida counties, your current plan might not be available at your new address. You generally have two full months after the month you move to choose a new Florida-specific plan. To avoid a gap in coverage, you should notify Medicare of your address change in Jensen Beach or Orlando as soon as possible. If you notify them before you move, your SEP begins the month before you relocate and lasts for two months after you arrive. This ensures your new Florida pharmacy has your information ready the day you move in.

Disaster and Emergency Special Enrollment

Florida’s hurricane season often leads to FEMA disaster declarations. When the federal government declares a state of emergency, Medicare provides a safety net for those who missed an enrollment deadline because of the crisis. This “Hurricane SEP” is specifically for individuals who reside in an area where a federal, state, or local government entity has declared a disaster. If you were unable to make a plan selection during the Annual Enrollment Period due to a storm, you may qualify for an extension. You typically do not need to provide extensive documentation of your hardship; living in the affected county is often sufficient proof. A local agent can verify if a disaster SEP is currently active in your specific Florida county to help you regain your enrollment rights.

Other common triggers for an SEP in Florida include:

- Loss of Employer Coverage: If you retire or lose COBRA coverage, you have 63 days to enroll in a standalone PDP to avoid late enrollment penalties.

- Qualifying for Extra Help: If you receive the Low-Income Subsidy (LIS), you can change your drug plan once per calendar quarter during the first nine months of the year.

- Moving into a Facility: Relocating into or out of a long-term care facility or nursing home opens a permanent SEP for the duration of your stay plus two months after you leave.

Understanding these rules ensures you never pay more than necessary for your medications. If you believe you qualify for one of these exceptions, reach out for a no-obligation review. Our licensed agents can help you secure your new plan quickly and accurately to maintain your peace of mind.

Step-by-Step: How to Enroll in a Florida Part D Plan

The 2026 medicare pdp enrollment period is your window to secure prescription drug coverage that fits your budget. To start, you’ll need a complete list of your current medications including exact dosages. This list is the foundation for any accurate plan comparison. Without it, you’re essentially guessing which plan provides the best value.

Next, review the 2026 formularies for major Florida carriers like Humana, UnitedHealthcare (UHC), and Florida Blue. Every carrier updates their list of covered drugs annually. A plan that worked for you in 2025 might move your specific medication to a higher tier in 2026. This simple change could significantly increase your monthly expenses.

Don’t focus solely on the monthly premium. You should calculate your total annual out-of-pocket cost. This includes the premium, the annual deductible, and your expected co-pays. For 2026, the standard deductible is capped at $590; however, some plans may offer a $0 deductible on Tier 1 and Tier 2 drugs. A plan with a $0 premium might actually cost you more over 12 months if the co-pays for your specific maintenance drugs are high.

Comparing Florida Plan Formularies

Formularies are tiered lists that determine your costs. For example, Plan A might classify a common heart medication as a Tier 2 drug with a low co-pay, while Plan B places it on Tier 4. These differences can result in hundreds of dollars in savings. Understanding these tiers is vital before you commit during the medicare pdp enrollment period. You can find more details on how these structures work by visiting our guide on Medicare Part D Plans.

Local Pharmacy Networks in Florida

Your choice of pharmacy is just as important as your choice of plan. Most Florida plans use preferred and standard pharmacy networks. You’ll typically pay less at preferred locations like Publix or certain CVS and Walgreens locations. If you’re one of the many Florida snowbirds who travel between the Treasure Coast and the North, ensure your plan offers robust mail-order options. For residents in Jensen Beach, using local pharmacies can often provide better pricing on Tier 1 and Tier 2 generics through established network contracts.

Finally, complete your enrollment with a licensed Florida Medicare agent. This ensures your application is processed correctly and that you’ve considered every available local option. A local expert can verify that your preferred neighborhood pharmacy is in-network and that your specific prescriptions are covered at the lowest possible cost.

Simplifying the Process: Why Work with a Florida Medicare Broker?

Choosing a prescription drug plan shouldn’t feel like a solo mission. While the federal government provides the framework for coverage, the local application of these plans varies significantly across the Sunshine State. Working with a licensed Florida Medicare broker offers a distinct advantage over high-pressure national call centers. These local experts provide personalized guidance without charging you a fee. Brokers receive compensation directly from insurance carriers, which means you get professional advice at no cost to your household budget. This client-first approach ensures your long-term health outcomes remain the priority rather than a quick sales quota.

A local consultant stays by your side even after you sign up. If your medications change in mid-2026 or you relocate to a different Florida county, you won’t have to navigate the bureaucracy alone. Your broker acts as a steady, reliable neighbor who understands the specific pharmacy networks and regional cost differences that national databases might overlook. This ongoing support provides peace of mind that your coverage will adapt as your life changes.

Local Knowledge vs. National Databases

National databases often miss the nuances of Florida’s provider networks. A Florida-based agent understands which pharmacies in cities like Orlando, Tampa, or Jacksonville offer the best preferred cost-sharing. They know the local healthcare landscape because they live and work in these communities. Whether you prefer a personalized phone consultation or a digital review, the goal is total clarity. You can explore your options through the Florida Medicare Advantage Home page to connect with a licensed agent who understands your specific zip code.

Your 2026 Medicare PDP Checklist

Missing a deadline can result in late enrollment penalties that stay with you for life. Keep these key 2026 dates on your calendar to ensure your coverage remains uninterrupted. The medicare pdp enrollment period serves as the essential gateway to affordable medication in Florida. Acting before the December 7 deadline ensures your new benefits begin on January 1, 2026.

- October 1, 2026: Start reviewing the Annual Notice of Change (ANOC) from your current provider.

- October 15, 2026: The Annual Election Period begins; you can officially start switching plans.

- December 7, 2026: The final day to enroll in or change your PDP for the upcoming year.

- January 1, 2027: Your new coverage and updated formulary officially take effect.

Don’t wait until the final week of the medicare pdp enrollment period to compare your options. Prescription costs can fluctuate, and a plan that worked in 2025 might not be the most cost-effective choice for 2026. Reach out for a no-obligation review today to ensure you’re getting the maximum savings available under Florida law.

Secure Your 2026 Florida Prescription Coverage

Navigating your prescription drug options for the upcoming year doesn’t have to be a source of stress. The medicare pdp enrollment period provides a vital window from October 15 through December 7 to ensure your 2026 coverage matches your health needs. Missing these federal deadlines can lead to permanent late enrollment penalties that increase your monthly costs by 1% for every month you went without creditable coverage. Our licensed Florida agents specialize in local market dynamics, offering access to top-rated carriers like Florida Blue and Humana. We provide personalized formulary reviews to ensure your specific medications are covered while maximizing your annual savings. Whether you’re entering your Initial Enrollment Period or qualifying for a 60-day Special Enrollment Period due to a move, professional guidance simplifies the transition. Taking these steps now ensures you aren’t overpaying for essential medicine next year.

Schedule your no-obligation Florida Part D review with a local expert today!

You’ve worked hard for your retirement, and securing the right healthcare is the best way to protect it. We’re here to help you move forward with confidence and clarity.

Frequently Asked Questions

Is there a deadline to sign up for Medicare Part D in Florida?

Yes, the primary deadline for the medicare pdp enrollment period is December 7 each year during the Annual Enrollment Period. If you’re turning 65, you have a 7-month Initial Enrollment Period that includes the three months before, the month of, and the three months after your birthday month. Missing these windows can result in a permanent late enrollment penalty.

Florida seniors should review their options early to ensure coverage begins on January 1, 2026. Working with a local licensed agent can help you track these dates so you don’t miss your chance to secure a plan.

What happens if I miss the Medicare PDP enrollment period?

You generally must wait until the next Annual Enrollment Period starting October 15 to secure a plan. During this gap, you’ll pay full retail price for your prescriptions at Florida pharmacies. This can lead to high out of pocket costs if you require maintenance medications for chronic conditions.

Additionally, Medicare adds a 1% penalty to your monthly premium for every full month you were without creditable coverage. This penalty stays with you for as long as you have Medicare drug coverage. It’s a permanent cost increase that follows you even if you switch plans later.

Can I change my drug plan at any time during the year in Florida?

No, you can only change your drug plan during specific windows like the Annual Enrollment Period or a Special Enrollment Period. The Medicare Advantage Open Enrollment Period from January 1 to March 31 also allows those with a Medicare Advantage plan to switch to Original Medicare and add a standalone PDP.

Outside of these dates, your 2026 plan selection remains locked for the duration of the calendar year. This is why a no-obligation review of your current medications is essential before the December 7 deadline passes.

How do I know if I qualify for a Special Enrollment Period in Florida?

You qualify for a Special Enrollment Period if you experience a life event such as moving to a new Florida county or losing employer-based drug coverage. Other triggers include moving into a long-term care facility or qualifying for financial assistance programs. Most SEPs last for 60 days from the date of the qualifying event.

A local licensed agent can verify your eligibility for these unique windows to ensure you don’t lose coverage. We provide the clarity you need to navigate these regulatory requirements without the stress of doing it alone.

Do all Florida Medicare Advantage plans include drug coverage?

Not all Medicare Advantage plans include prescription drug benefits, though approximately 89% of plans offered in Florida do provide this coverage. Plans that include drugs are known as MAPDs. If you choose a Florida Medicare Advantage plan without drug coverage, you generally cannot buy a separate standalone PDP.

It’s vital to check the specific Summary of Benefits for any plan you’re considering for 2026. Our team helps you compare these plan differences to ensure your specific medications are on the plan formulary.

How much is the late enrollment penalty for Part D in 2026?

The penalty is calculated by multiplying 1% of the national base beneficiary premium by the number of full, uncovered months you were eligible but didn’t enroll. In 2025, this base premium was $34.70, and CMS updates this figure annually. The total is rounded to the nearest $.10 and added to your monthly premium indefinitely.

This cost applies even if you move between different Florida drug plans in the future. Avoiding this penalty is a key part of maintaining a stable budget on a fixed income.

Can I have both a Medicare Supplement and a Part D plan in Florida?

Yes, pairing a Florida Medicare Supplement plan with a standalone Part D plan is a common way to get comprehensive coverage. Medigap plans don’t cover outpatient prescription drugs, so a separate PDP is necessary to avoid the late enrollment penalty. This combination allows you to use any doctor in Florida who accepts Medicare while maintaining predictable costs for your medications.

Many seniors prefer this setup because it offers a sense of security and broad access to providers. We can help you find a drug plan that complements your supplement for total peace of mind.

What is ‘Extra Help’ and how does it affect my enrollment window?

Extra Help is a federal program that assists seniors with limited income in paying for Part D premiums and co-pays. If you qualify, you’re granted a Special Enrollment Period that allows you to change your medicare pdp enrollment period choices once per calendar quarter during the first nine months of the year.

This provides significant flexibility for Florida residents to adjust their coverage as their health needs or financial situations change. If you think you might qualify, speaking with a local expert can help you start the application process today.