For the first time in the history of the program, your annual out-of-pocket prescription costs will be strictly capped at $2,000 starting in 2026. This landmark change provides a new level of financial security, yet the florida medicare part d enrollment process remains a source of stress for many seniors. You probably agree that choosing between a Stand-alone Prescription Drug Plan and a Medicare Advantage Plan feels like a high-stakes guessing game. The fear of a lifetime late enrollment penalty only adds to the pressure when you’re trying to protect your retirement savings.

Our local experts are here to replace that anxiety with clear, actionable guidance. We promise to help you secure the lowest possible monthly premiums while ensuring your neighborhood Florida pharmacy stays in-network. This guide explains the latest 2026 cost-sharing updates and provides a step-by-step timeline to help you meet every deadline. You’ll learn how to avoid common mistakes and find a plan that protects both your health and your peace of mind.

Key Takeaways

- Understand the vital differences between standalone PDP and MAPD plans to choose the right prescription coverage for your 2026 health needs.

- Navigate the florida medicare part d enrollment process with confidence by mastering the key deadlines for the Initial and Annual Enrollment Periods.

- Learn how to evaluate your current medications and local pharmacy networks, such as CVS or Publix, to identify the most cost-effective plan options.

- Discover why a no-obligation review with a local Florida licensed agent provides more personalized savings than a national call center.

- Prepare for the 2026 prescription drug cost changes and secure your peace of mind with expert guidance tailored to the Florida market.

Understanding Medicare Part D in Florida for 2026

Medicare Part D is the federal government’s way of helping you pay for prescription drugs. While it’s technically optional, skipping it often leads to lifelong penalties that increase your monthly costs. For residents of the Sunshine State, Medicare Part D provides a layer of security that Original Medicare (Part A and Part B) simply doesn’t offer on its own. You’ll find these plans offered by private insurance companies that Medicare approves. These plans work alongside your existing coverage to lower the price of both generic and brand-name drugs at your local pharmacy.

Even if you don’t take medications today, completing your florida medicare part d enrollment during your initial window is a smart move. Health needs can change quickly. Securing coverage now ensures you won’t face a late enrollment penalty if you need to join a plan later in life. It’s about protecting your future budget and gaining peace of mind. Our local experts often see seniors surprised by how much they save just by having a plan in place before a health event occurs.

To better understand how these plans work for you, watch this helpful video from Florida Blue:

The 2026 Prescription Drug Cost Revolution

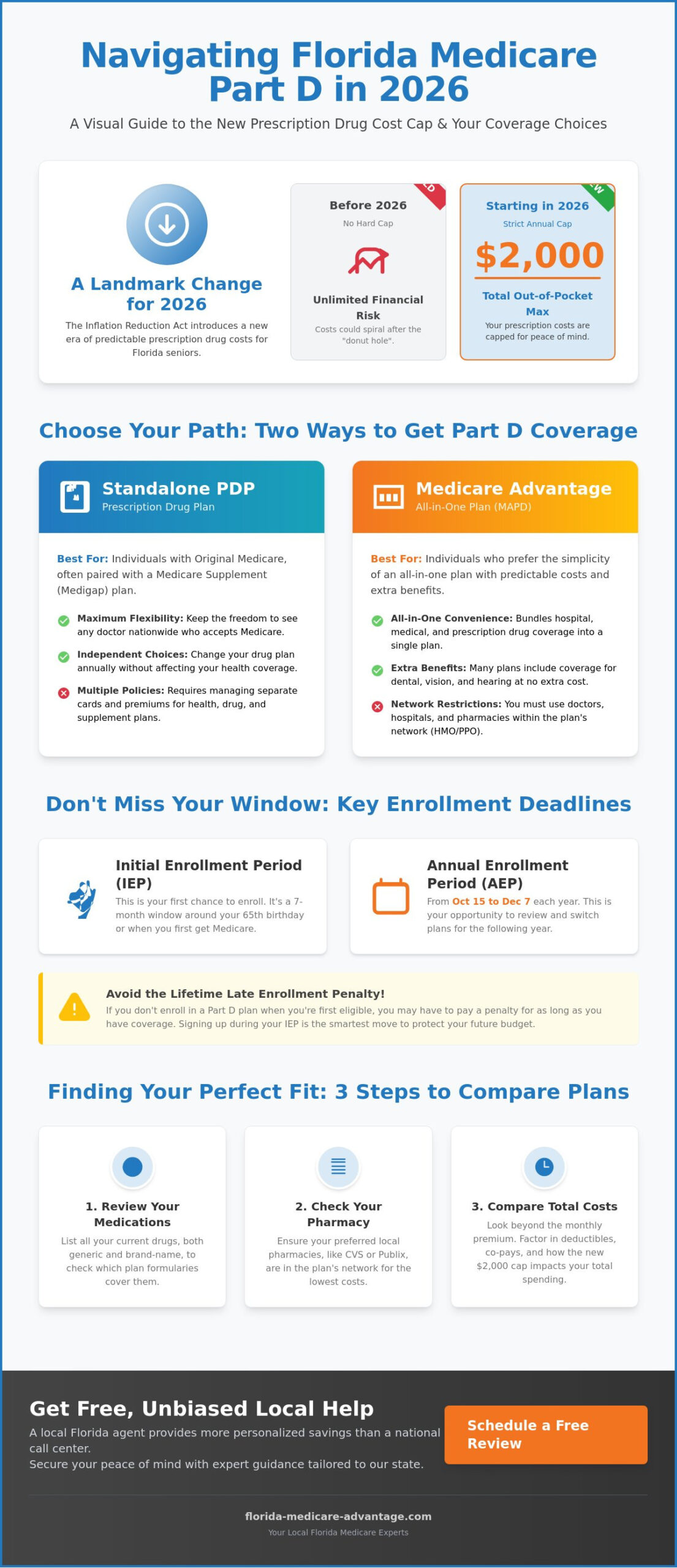

The year 2026 marks a historic shift for Florida beneficiaries due to the Inflation Reduction Act. The most significant change is the total elimination of the “donut hole” or coverage gap. This confusing phase of coverage used to leave many seniors responsible for a higher percentage of their drug costs mid-year. Starting January 1, 2026, the new law simplifies everything. This $2,000 cap ensures that no Florida senior will face unlimited financial liability for life-saving medications. This change provides predictable costs and genuine financial safety for those on fixed incomes.

Who is Eligible for Florida Part D?

To begin your florida medicare part d enrollment, you must first be entitled to Medicare Part A or enrolled in Medicare Part B. You also have to live in the service area of the plan you choose. Florida-specific plans are designed for residents with a permanent address in the state, ensuring the network includes the pharmacies you already use. If you have limited income, you might qualify for “Extra Help” or Medicaid. These programs can significantly lower your premiums and co-pays. Our licensed agents can help you determine if you’re eligible for these additional savings. Choosing the right plan requires a careful look at your current prescriptions and your preferred local pharmacy. This local expertise helps you avoid the high-pressure tactics of national call centers.

Comparing Florida Part D Options: Standalone PDP vs. MAPD

Choosing the right path for your florida medicare part d enrollment depends on how you prefer to receive your medical benefits. You essentially have two distinct routes: keeping Original Medicare with a standalone plan or moving to a private Medicare Advantage plan. Before you can select either, you must be enrolled in Medicare Parts A and B. You can find detailed instructions on this initial step in the Social Security Administration’s Medicare Enrollment Guide. Once your basic Medicare is active, you can decide which drug coverage structure fits your lifestyle.

Standalone Prescription Drug Plans (PDP)

Standalone PDPs are specifically designed for those who choose to stay with Original Medicare. This path is the standard choice if you also have one of the many Medicare Supplement plans available in the state. These plans give you the freedom to see any doctor in the country who accepts Medicare while adding a separate policy for your prescriptions.

In the Florida market, monthly premiums for standalone PDPs can vary significantly. While some basic plans might start at very low rates, others with more robust formularies can exceed $100. The primary benefit here is flexibility. You aren’t tied to a specific health network; you simply choose the plan that covers your specific medications at the lowest total cost. This allows you to switch drug plans annually during the Open Enrollment Period without affecting your secondary health insurance.

Medicare Advantage Prescription Drug (MAPD) Plans

Many Florida seniors prefer the convenience of Medicare Advantage plans that include drug coverage. These “all-in-one” options combine your hospital, medical, and pharmacy benefits into a single plan. You’ll use one member ID card at both the doctor’s office and the pharmacy counter, which simplifies your record-keeping. The 2026 landscape offers several paths for florida medicare part d enrollment, each catering to different health and budget priorities.

For 2026, many Florida counties continue to offer MAPD plans with $0 monthly drug premiums. This doesn’t mean the drugs are free, but it eliminates the extra monthly bill associated with a standalone policy. Before committing, you should follow these steps:

- Verify your current Florida doctors are in the plan’s network.

- Confirm your specific prescriptions are on the plan’s formulary.

- Check for “preferred” pharmacy locations in your local neighborhood.

- Compare the total out-of-pocket maximums for medical services.

This bundled approach is often the most cost-effective for those on a fixed income. If you’re feeling overwhelmed by the choices, a no-obligation review with a local agent can clarify which network includes your preferred specialists and medications.

Florida Enrollment Periods and Key Deadlines

Timing your florida medicare part d enrollment correctly prevents coverage gaps and protects your budget from lifelong surcharges. Medicare operates on a strict calendar. Missing these windows often means waiting until the next year to secure the prescriptions you need. Most residents begin their journey during the Initial Enrollment Period (IEP). This seven month window centers around your 65th birthday, including the three months before, your birth month, and the three months after. If you are turning 65 in Florida, this is your primary opportunity to select a plan without health questions or penalties.

Once you are in the system, you must monitor the annual windows. The most active time for plan changes is the Annual Enrollment Period (AEP). This runs from October 15 through December 7 every year. During this time, you can add, drop, or switch your standing drug coverage for the upcoming 2026 plan year. Changes made during AEP take effect on January 1. If you currently have a Medicare Advantage plan, you also have access to the Medicare Advantage Open Enrollment Period (MAOEP). From January 1 to March 31, you can leave your current Advantage plan, return to Original Medicare, and select a standalone Part D plan.

Keeping track of these dates is easier with a Medicare Deadline for Enrollment 2026 Guide. Local experts suggest marking these dates on a physical calendar to avoid the last minute rush that often happens in early December.

The Cost of Waiting: Late Enrollment Penalties

Delaying your florida medicare part d enrollment results in a permanent financial penalty unless you have “creditable” coverage. This is insurance that pays out at least as much as a standard Medicare drug plan. The Center for Medicare Advocacy notes that the penalty is calculated as 1% of the national base beneficiary premium for every full month you were eligible but did not enroll. For 2024, the base premium is $34.70. If you wait 24 months to join, you will pay an extra 24% on top of your monthly premium for as long as you have drug coverage. This cost follows you even if you switch plans or move to a different state.

Special Enrollment Periods (SEP) for Florida Residents

Life changes often trigger a Special Enrollment Period, allowing you to modify your coverage outside the standard windows. Florida residents frequently qualify for an SEP after moving to a new county or transitioning out of employer sponsored health plans. If you lose your job based coverage, you generally have 63 days to find a Part D plan before a penalty begins to accrue. Financial changes also create opportunities. If you qualify for the Florida Extra Help program, also known as the Low Income Subsidy, you may be able to change your plan once per quarter during the first nine months of the year. You can find more details in our Medicare PDP Enrollment Period 2026 Guide.

How to Compare Plans and Enroll in Florida

Choosing the right coverage requires a methodical approach to ensure your specific health needs align with your budget. The florida medicare part d enrollment process is most successful when you follow a clear, four-step strategy designed to eliminate surprises at the pharmacy counter.

- Step 1: Gather your medication list. Document every prescription, including exact dosages and the frequency of your refills. Accuracy here prevents choosing a plan that excludes a vital medication.

- Step 2: Check pharmacy network status. Major Florida retailers like Publix, CVS, and Walgreens often have different cost-sharing levels depending on the plan. A “preferred” status can save you hundreds of dollars annually compared to a “standard” status.

- Step 3: Review the plan formulary. A formulary is the list of drugs a plan covers. You must verify that your specific medications are listed and check which cost tier they occupy.

- Step 4: Calculate the Total Annual Cost. Do not choose a plan based on the monthly premium alone. Add the annual premium to your estimated deductible and your expected copays to find the true price of the plan.

Florida residents often find that plans with the lowest premiums have the highest out-of-pocket costs when they actually fill a prescription. Our licensed agents can help you run these numbers to ensure your 2026 coverage provides genuine peace of mind.

Navigating Plan Formularies and Tiers

Medicare Part D plans in Florida categorize drugs into tiers, which determine your share of the cost. Tier 1 usually consists of preferred generics with the lowest copays, while Tier 5 contains specialty drugs for complex conditions. Many Florida plans also implement “Prior Authorization,” where your doctor must prove a drug is medically necessary before the plan pays. You might also encounter “Step Therapy,” which requires you to try a more affordable drug before the plan covers a more expensive option.

Evaluating Florida Pharmacy Networks

Your choice of pharmacy significantly impacts your wallet. Preferred network pharmacies offer the lowest negotiated rates, while standard pharmacies charge higher out-of-pocket amounts. For those living in rural Florida counties, checking local independent pharmacies in your specific zip code is essential, as some plans specialize in local access. Many seniors find that mail-order options provide the best value for 90-day supplies of maintenance medications, often reducing three copays down to two. This is a simple way to protect your fixed income.

Ready to find the most cost-effective coverage for your medications? Speak with a local expert for a no-obligation review of Florida Medicare Part D plans today.

Get Expert Help with Your Florida Part D Plan

Choosing a prescription drug plan involves more than just looking at a monthly premium. It’s about ensuring your specific medications are covered at a price you can afford. A local Florida licensed insurance agent provides a level of precision that national call centers often lack. These local experts understand the nuances of the Florida market, offering you direct access to plans from top-rated carriers including Florida Blue, Humana, and UnitedHealthcare. By working with someone who lives and works in the same state, you gain a partner who prioritizes your long-term health over a quick enrollment.

Managing your healthcare should feel secure, not stressful. A local broker acts as a steady guide, helping you compare the 2026 plan changes against your actual medication needs. This personalized approach often reveals cost-saving opportunities that automated systems might overlook. Whether it is finding a plan with a lower deductible or identifying a pharmacy with better preferred cost-sharing, local expertise makes a measurable difference in your annual out-of-pocket costs.

Why a Local Florida Broker Matters

Florida’s healthcare landscape is unique. A local broker understands which regional pharmacy networks, such as those found in Publix or local independent pharmacies, offer the best savings in your specific ZIP code. They know how local medical groups interact with different carriers across the state. This expertise is vital during the 2026 florida medicare part d enrollment period, as plan formularies and tier structures change every year. Your service doesn’t end when you sign up. A dedicated agent remains available to help you navigate coverage gaps or unexpected billing issues throughout the year. You can learn more about Part D plans and how they integrate with your current coverage to ensure there are no gaps in your care.

Next Steps: Schedule Your No-Obligation Review

Securing your 2026 coverage starts with a clear look at your current medication list. A no-obligation review can identify significant savings, especially if a lower-cost generic has become available or if your current plan’s premium is increasing for the new year. To make the most of your consultation with a Florida Medicare Advantage expert, have the following items ready:

- A complete list of your current prescriptions, including exact dosages and frequency.

- Your preferred pharmacy name and location to check for network status.

- Your Medicare card to verify your current enrollment dates and ID numbers.

Taking these steps now prevents the stress of last-minute changes during the busy florida medicare part d enrollment season. Our team focuses on a client-first approach, ensuring you feel confident and secure in your choices for the coming year. Speak with a local Florida Medicare expert today to begin your personalized review and find the peace of mind you deserve.

Secure Your 2026 Prescription Savings Today

Navigating your florida medicare part d enrollment for the 2026 season requires careful attention to the Annual Enrollment Period, which runs from October 15 through December 7. You’ve seen how choosing between a standalone Prescription Drug Plan and a Medicare Advantage plan impacts your pharmacy access and monthly budget. It’s vital to review your formulary every year because carrier offerings from companies like Humana, UnitedHealthcare, and Florida Blue frequently update their covered medications. Missing these specific deadlines often means waiting another full year to adjust your coverage, which can lead to higher out-of-pocket costs.

You don’t have to manage these complex federal regulations alone. Our team consists of licensed Florida insurance agents who live and work in your community. We aren’t an impersonal national call center; we’re local experts dedicated to your long-term health outcomes. We provide the clarity you need to compare top-rated carriers and find a plan that fits your specific prescriptions. Take the first step toward peace of mind by requesting your Get a No-Obligation Florida Part D Plan Review. We’re here to ensure you feel confident and fully prepared for the year ahead.

Frequently Asked Questions

When is the Florida Medicare Part D enrollment period for 2026?

You can complete your Florida Medicare Part D enrollment during the Annual Enrollment Period, which runs from October 15 through December 7, 2025. This window allows you to secure coverage that begins on January 1, 2026. If you’re new to the program, your Initial Enrollment Period starts three months before you turn 65 and lasts for seven months total.

Can I change my Part D plan if I move to a different county in Florida?

You can switch your plan if you move to a new county because Medicare grants a Special Enrollment Period for relocation. This window typically lasts for two full months after the month you move. If you notify your plan provider before you move, your new coverage can begin as early as the first day of the month you arrive in your new Florida home.

Is there a penalty if I don’t enroll in Part D when I first turn 65?

You’ll face a permanent late enrollment penalty if you go 63 days or more without creditable drug coverage after your initial eligibility ends. The Social Security Administration calculates this penalty as 1% of the national base beneficiary premium for every full month you were eligible but didn’t enroll. This cost is added to your monthly premium for as long as you have a Medicare drug plan.

What is the $2,000 out-of-pocket cap for 2026 Part D plans?

Starting in 2025 and continuing through 2026, the Inflation Reduction Act caps your annual out-of-pocket prescription costs at $2,000. This federal law eliminates the “donut hole” coverage gap entirely, providing financial relief for seniors with high medication expenses. Once you reach this $2,000 limit, you won’t pay any out-of-pocket costs for covered drugs for the remainder of the calendar year.

How do I know if my medications are covered by a Florida Part D plan?

You should review the plan’s formulary, which is a formal list of covered drugs organized into cost tiers. Every insurance provider must update this list annually to reflect current clinical guidelines and pricing. Our licensed agents can perform a no-obligation review of your current medications to ensure they’re included in a 2026 plan’s coverage list before you commit to any florida medicare part d enrollment.

Can I have both a Medicare Advantage plan and a separate Part D plan?

You generally can’t have both a standalone Part D plan and a Medicare Advantage plan that already includes drug coverage. If you’re enrolled in a Medicare Advantage (Part C) plan, your prescription benefits are typically bundled into that single policy. Attempting to buy a separate drug plan while holding an Advantage plan could result in being automatically disenrolled from your health coverage and returned to Original Medicare.

What is the Extra Help program for Florida Medicare beneficiaries?

Extra Help is a federal program that assists seniors with limited income in paying for their Part D premiums, deductibles, and coinsurance. In 2024, the Social Security Administration estimated this benefit is worth approximately $5,900 annually per person. Florida residents who qualify for this Low Income Subsidy don’t face late enrollment penalties and can switch their drug plans once per quarter during the first nine months of the year.

Do I need Part D if I have drug coverage through the VA?

You don’t need to enroll in Part D if you have prescription coverage through the Department of Veterans Affairs, as VA benefits are considered creditable coverage. This means you won’t face a late enrollment penalty if you decide to join a private drug plan later. Many Florida veterans still choose to enroll in a Part D plan to access local pharmacies that aren’t part of the VA network.