Last October, a retiree in Sarasota discovered that missing a single seven-day window could result in a 10% lifelong penalty on their Medicare Part B premiums. It’s a stressful realization that many neighbors face when trying to track the various medicare enrollment periods without local guidance. These federal deadlines are rigid, and a simple misunderstanding of the 2026 calendar can lead to gaps in coverage that last for an entire year.

You likely find the distinction between the fall Annual Enrollment Period and the winter Open Enrollment Period more confusing than it needs to be. It’s natural to worry about how a move to the Sunshine State might disrupt your current benefits or trigger new requirements. Our goal is to replace that uncertainty with the steady confidence of an expert plan. This guide outlines the essential 2026 dates, explains how to qualify for special exceptions, and ensures you have a clear path to the savings you deserve. If you ever feel overwhelmed, you can always speak with a local expert for a no-obligation review of your specific situation.

Key Takeaways

- Identify the critical seven-month window surrounding your 65th birthday to secure essential coverage and avoid lifelong late enrollment penalties.

- Learn how to navigate the Annual Enrollment Period and the “second chance” window to ensure your plan benefits align with your 2026 health goals.

- Discover how specific life changes or local emergencies can qualify you for special medicare enrollment periods, providing flexibility outside of standard dates.

- Gain the peace of mind that comes from working with a local Jensen Beach expert who understands the nuances of Florida-specific provider networks.

Understanding Medicare Enrollment Periods in Florida

Medicare enrollment periods aren’t just dates on a calendar; they’re your primary safeguard against lifelong costs. These specific windows allow you to join, switch, or drop coverage as your health needs evolve. Since the inception of Medicare (United States) in 1965, the system has grown to include complex choices between Original Medicare and private alternatives. In 2026, Florida seniors have more local plan options than ever, making the timing of your application a critical factor in your long-term financial health.

To get a clear picture of how these timelines work in 2026, watch this helpful breakdown:

Why Timing Matters for Florida Seniors

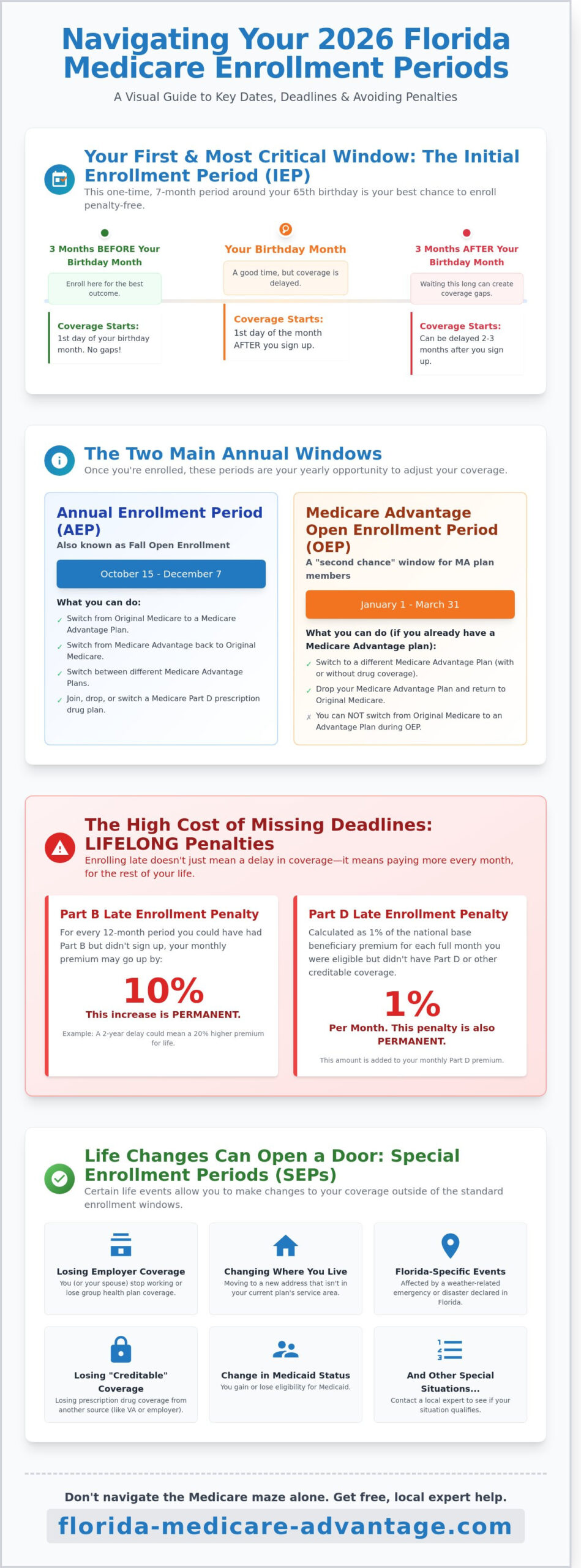

Missing a deadline can be a permanent financial mistake. If you miss your initial window for Part B, you’ll face a 10% penalty for every 12-month period you were eligible but didn’t sign up. This penalty stays with you for life. Part D carries a similar 1% monthly penalty for late enrollment. In 2026, Florida seniors in regions like Martin County will see a 12% increase in local plan availability compared to previous years. These shifts mean that yesterday’s plan might not be today’s best value. A local licensed agent can track these medicare enrollment periods for you at no cost, ensuring you never pay more than necessary.

The Four Main Enrollment Windows

The Medicare calendar rests on four pillars that determine when you can access benefits. If you’re turning 65 and exploring Medicare options, the Initial Enrollment Period (IEP) is your first and most vital window. Other pillars include:

- Annual Enrollment Period (AEP): Runs from October 15 to December 7 each year.

- Medicare Advantage Open Enrollment Period (OEP): Occurs from January 1 to March 31.

- Special Enrollment Periods (SEP): Triggered by life events like moving to a new Florida zip code.

When you enroll during these medicare enrollment periods, your coverage always begins on the first of the month following your application. It’s a structured process designed to ensure you’re never without protection. You don’t have to navigate these rules alone. Our local experts provide the clarity you need to move forward with confidence and peace of mind.

Your Initial Enrollment Period (IEP): Turning 65 in Jensen Beach

For seniors on the Treasure Coast, the Initial Enrollment Period (IEP) is the most critical of all medicare enrollment periods. It’s your first opportunity to secure coverage without facing late enrollment penalties or health screenings. This window lasts exactly seven months, centered around the month you turn 65. Missing this timeframe can lead to permanent increases in your Part B premiums and may limit your access to certain Medigap plans later. It’s the ideal time to explore options for turning 65 to ensure your transition is seamless.

The 7-Month IEP Timeline

Success starts with understanding the three distinct phases of your enrollment window. Your coverage start date depends entirely on when you act:

- The Early Bird Window: This includes the three months before your 65th birthday month. Enrolling now ensures your benefits begin on the first day of your birth month.

- The Birthday Month: Signing up during the month you turn 65 is common, but it may cause a slight delay in the start of your coverage.

- The Final Window: You have three months after your birthday month to finish your application. Be aware that waiting until this phase can result in a coverage gap of two to three months.

What if You Are Still Working at 65?

Many Florida residents continue working well past 65 and maintain employer-sponsored health insurance. If your company has 20 or more employees, your current group coverage is likely considered “creditable” by Social Security standards. This allows you to delay Part B without penalty. However, if your employer has fewer than 20 employees, Medicare usually becomes your primary payer at age 65. In this case, you must enroll during your IEP to avoid a lifetime 10% late enrollment penalty for every 12-month period you were eligible but didn’t sign up.

A recent KFF analysis of enrollment periods highlights how complex these choices are, especially when comparing traditional Medicare with Medicare Advantage. If you’re unsure if your current workplace plan qualifies as creditable, you can speak with a local expert to verify your status and protect your future rates. Decisions made during these medicare enrollment periods stay with you for years, so getting the facts early provides essential peace of mind.

Annual Windows: AEP and Medicare Advantage Open Enrollment

Understanding the calendar is the first step toward securing your health coverage for 2026. While some medicare enrollment periods only happen once in a lifetime, others return every year to allow for plan adjustments. These annual windows are the best time to compare Medicare Advantage plans to see if your current coverage still meets your budget. You can also use these times to add or change Medicare Part D drug plans to ensure your prescriptions remain affordable. Our licensed agents recommend marking these dates on your calendar to avoid missing out on potential savings.

The Annual Enrollment Period (Oct 15 – Dec 7)

The Annual Enrollment Period (AEP) acts as the primary window for most Florida seniors. Starting October 15, you can switch from Original Medicare to a Medicare Advantage plan or move between different Advantage options. It’s a critical time because insurance carriers frequently update their terms. For instance, providers like Florida Blue or Humana might adjust their provider networks in Martin County for the 2026 plan year. You should receive your Annual Notice of Change (ANOC) by September 30. This document details every change in your premiums, copays, or benefits. Reviewing it carefully ensures you aren’t surprised by new costs on January 1. If your current plan’s drug list changes, medicare enrollment periods like AEP allow you to find a more cost-effective alternative. We provide a no-obligation review to help you interpret these changes quickly.

Medicare Advantage Open Enrollment (Jan 1 – Mar 31)

If you start the new year and realize your plan isn’t a perfect fit, the Medicare Advantage Open Enrollment Period (MA OEP) provides a safety net. This window is specifically for residents already enrolled in a Medicare Advantage plan as of January 1. You get one chance to make a change during these three months. You can switch to a different Advantage plan or return to Original Medicare. If you choose to go back to Original Medicare, you can also join a standalone Part D plan at that time. This period offers peace of mind for those who find their doctor is no longer in-network or their monthly costs have increased unexpectedly. It’s a “second chance” to ensure your Florida healthcare coverage aligns with your actual needs rather than just your initial expectations.

Special Enrollment Periods (SEP): Life Changes and Florida Emergencies

Life doesn’t always follow a set schedule. While the standard medicare enrollment periods provide fixed dates for coverage changes, Special Enrollment Periods (SEPs) offer a vital safety net for unexpected transitions. These windows allow you to adjust your health plan outside of the usual fall or winter dates. Most SEPs last for 60 days following a qualifying event, ensuring you don’t face a gap in coverage or late enrollment penalties during a major life change.

Common triggers for an SEP include:

- Losing your current health coverage, such as through retirement or the end of a COBRA plan.

- Moving your primary residence to a new service area.

- Qualifying for “Extra Help” to pay for prescription drug costs.

- Changes in your eligibility for Medicaid or “dual-eligible” status.

Understanding these rules is essential for maintaining your health security. A local agency can help you identify if you qualify for a specific enrollment exception based on your current situation.

Moving to Florida: The “Snowbird” or Permanent Resident Window

Moving to Jensen Beach from another state like New York or Ohio triggers a 2-month SEP. This window begins either the month before you move or the month you notify Medicare, whichever is later. You must choose a plan that covers your new Florida service area because Medicare Advantage networks are zip-code specific. It’s vital to distinguish between permanent moves and seasonal snowbird status. If you keep your primary residence in the north and only spend winters in Florida, you generally don’t qualify for a move-based SEP. Permanent residents must update their address with the Social Security Administration to activate this enrollment right.

FEMA and Hurricane SEPs in Florida

Florida seniors face unique risks from tropical weather. When a hurricane or tropical storm leads to a state-declared emergency, Medicare often provides additional flexibility for those who missed a deadline. The FEMA SEP acts as a grace period for individuals who were unable to meet an enrollment deadline because they lived in an area affected by a federally declared natural disaster. This extension typically applies to all 67 Florida counties if the disaster declaration is statewide. To document your eligibility, you usually only need to provide proof of residency in an affected county during the incident period. This protection ensures that a natural disaster doesn’t result in a permanent loss of health benefits or higher premiums.

If you’ve recently moved or been impacted by a storm, contact us for a no-obligation Florida Medicare review with a licensed expert today.

Navigating Deadlines: How a Jensen Beach Medicare Agent Can Help

Missing specific medicare enrollment periods often results in a lifetime of higher premiums and unexpected gaps in coverage. While national call centers handle thousands of callers, they rarely understand the specific nuances of Florida’s regional networks. A local Jensen Beach agent knows which plans include the specialists you trust at Cleveland Clinic Martin North or local independent practices. Our licensed agents provide a no-obligation review to ensure your 2026 coverage matches your health needs and budget. You can contact Florida Medicare Advantage today to secure your peace of mind before the next deadline arrives.

The complexity of federal regulations can be as daunting as navigating a major international waterway; for example, ship operators rely on the expert guidance of a firm like Adimar Shipping, Inc. to safely transit the Panama Canal. Similarly, local Medicare experts handle the heavy lifting of paperwork and verification, ensuring one small error doesn’t delay your benefits for months. We focus on your specific zip code to find benefits that national brokers might overlook. This direct, cause-and-effect approach replaces confusion with a clear path forward. You get the clarity of a face-to-face consultation without the high-pressure tactics used by large-scale insurance telemarketers.

The Advantage of Local Treasure Coast Expertise

National brokers often rely on generic databases that are frequently outdated. Local agents live in the community and understand which Jensen Beach doctors are currently accepting new patients under specific plans. This personalized service provides a level of detail that a “one-size-fits-all” script cannot match. We help Martin County seniors avoid the “late enrollment” trap by identifying the exact windows for their unique situations. This prevents the 10% Part B penalty that accumulates for every 12 month period you lacked coverage. Our goal is to ensure you stay in-network and on-budget throughout 2026.

Next Steps: Your 2026 Medicare Checklist

Preparation is the key to a stress-free experience. Before your next medicare enrollment periods arrive, you should complete these three practical steps:

- Gather your current plan information and a comprehensive prescription list, including exact dosages and frequencies.

- Mark your calendar with the 2026 AEP dates, which run from October 15 to December 7, to avoid last-minute decisions.

- Schedule a free consultation with a Jensen Beach agent to review your 2026 Evidence of Coverage documents as soon as they arrive in September.

Taking these steps early ensures you aren’t rushing through a decision that affects your health for the entire year. A local agent acts as a steady, reliable neighbor who understands the local healthcare landscape. We prioritize your long-term health outcomes over quick sales, giving you the confidence to make an informed choice for your future.

Take Control of Your 2026 Healthcare Future

Missing a deadline during specific medicare enrollment periods can lead to lifelong financial penalties or gaps in your medical coverage. Whether you’re turning 65 in Jensen Beach or need to make changes during the Annual Enrollment Period from October 15 to December 7, timing remains your most important asset. Our local office provides direct access to top-tier plans from Humana, UnitedHealthcare, and Florida Blue. We focus on your specific health requirements to find a plan that fits your budget and lifestyle. You deserve the clarity that comes from a face-to-face consultation with a professional who understands the Florida market inside and out.

Our licensed agents offer no-obligation, commission-based enrollment services to ensure your needs always come first. You don’t have to settle for a generic plan from a national call center. Instead, get the personalized attention you need to make an informed decision for the 2026 plan year. Speak with a Licensed Jensen Beach Medicare Agent today to secure the benefits you’ve earned. We’re here to help you move forward with total confidence.

Frequently Asked Questions

When is the Medicare enrollment period for 2026?

The primary Medicare enrollment period for 2026 begins with the Annual Election Period, which runs from October 15, 2025, through December 7, 2025. During these 54 days, Florida seniors can join, drop, or switch their Medicare Advantage or Part D prescription drug plans. If you miss this window, the General Enrollment Period provides another opportunity between January 1 and March 31, 2026, for those who need to sign up for Part A or Part B for the first time.

What happens if I miss the Medicare enrollment deadline in Florida?

Missing your enrollment deadline often results in a permanent late enrollment penalty that’s added to your monthly premium. For Part B, this penalty is a 10% increase for every full 12-month period you were eligible but didn’t sign up. These costs stay with you for the life of your coverage and can significantly impact a fixed income. Our licensed agents can help you identify if you qualify for a Special Enrollment Period to avoid these extra charges and secure your peace of mind.

Can I change my Medicare plan at any time if I move to Jensen Beach?

Moving to a new service area like Jensen Beach triggers a 2-month Special Enrollment Period that starts either the month before you move or the month you notify Medicare. This window allows you to switch to a plan available in Martin County without waiting for the fall season. Since plan benefits and provider networks vary by Florida zip code, a no-obligation review ensures your new coverage includes your preferred local doctors and pharmacies. It’s a simple way to maintain continuity of care during your transition.

Is there a special enrollment period for Florida hurricanes?

Florida residents often qualify for a Special Enrollment Period when the Governor or FEMA declares a state of emergency due to a hurricane or other natural disaster. This extension typically grants an additional 4 months from the start of the incident to make plan changes if you missed a deadline because of the storm. In 2024, thousands of seniors utilized this provision following major weather events to protect their health coverage. You should speak with a local expert to verify if a specific disaster has opened an enrollment window in your county.

How long is the Medicare Initial Enrollment Period when I turn 65?

Your Initial Enrollment Period lasts for exactly 7 months, centered around your 65th birthday month. This window includes the 3 months before your birth month, the month you turn 65, and the 3 months following. Enrolling during the first 3 months ensures your coverage starts on the first day of your birth month, preventing any gaps in your healthcare. If you miss this 7-month window, you’ll likely face lifetime penalties on your Part B premiums and may have to wait months for your next enrollment opportunity.

Do I need to re-enroll in Medicare every year?

You don’t need to re-enroll in your current plan every year because most Medicare Advantage and Part D plans renew automatically on January 1. However, insurance companies change their costs, provider networks, and drug formularies annually, which affects 100% of participants. We recommend a no-obligation review during the annual medicare enrollment periods to ensure your current plan still offers the best value for your specific needs. This proactive step prevents unexpected increases in your out-of-pocket maximums or prescription co-pays.

What is the difference between Open Enrollment and the General Enrollment Period?

The Open Enrollment Period from October 15 to December 7 is for people already in Medicare who want to change their existing coverage for the upcoming year. In contrast, the General Enrollment Period from January 1 to March 31 is specifically for those who didn’t sign up for Part A or Part B when they were first eligible. While Open Enrollment focuses on plan optimization and extra benefits, the General Enrollment Period serves as a second chance to secure basic coverage. Both are critical medicare enrollment periods that Florida seniors must track to maintain continuous and affordable health protection.