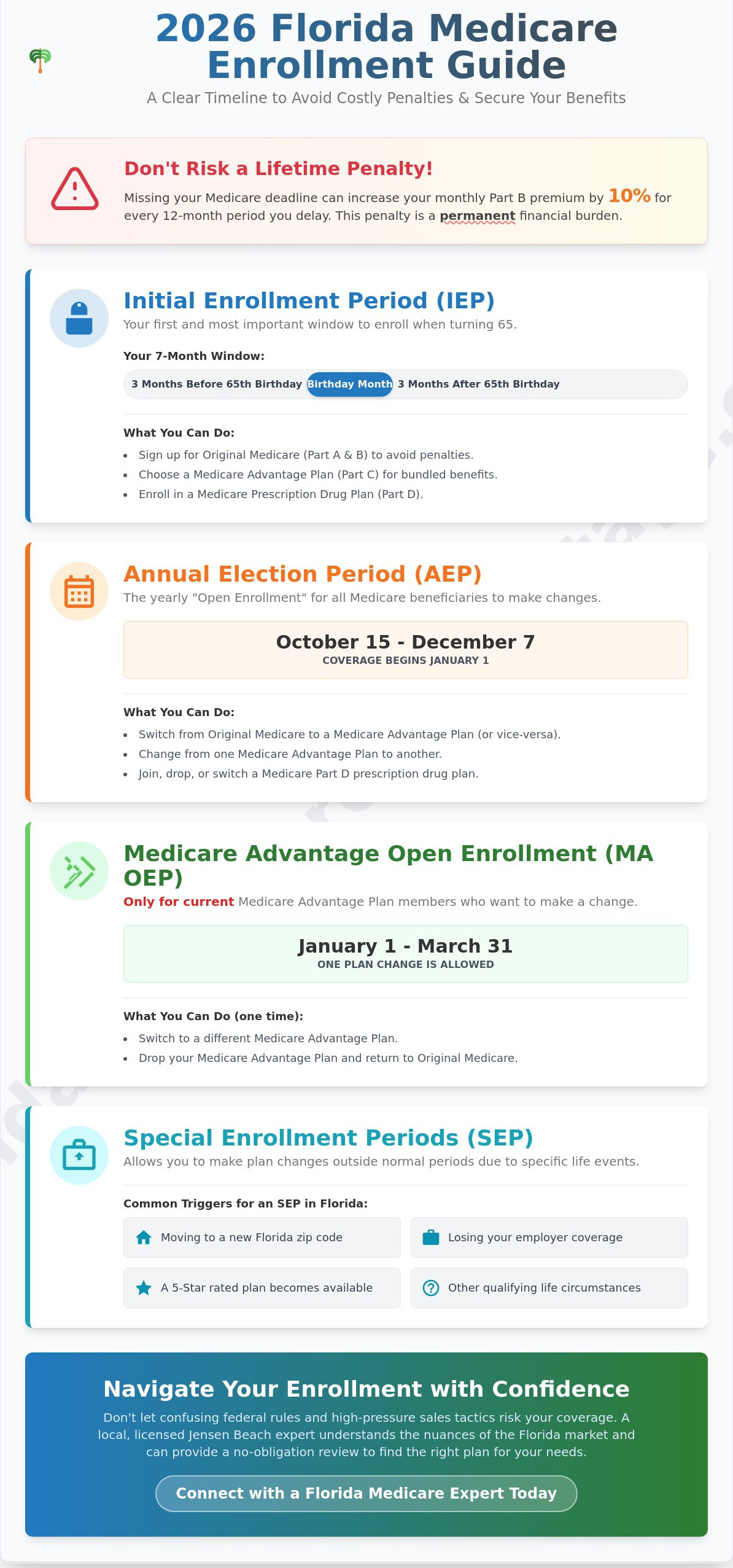

Missing a single Medicare deadline can result in a lifetime penalty that increases your monthly Part B premiums by 10% for every 12 month period you lacked coverage. It is a permanent financial burden that many Florida seniors don’t realize exists until the bill arrives. You’ve likely felt the mounting pressure from national call centers and confusing mailers filled with acronyms like IEP, AEP, and SEP. It’s frustrating to manage these complex federal rules while searching for a plan that actually works for your lifestyle here in the Sunshine State. Understanding exactly when is medicare enrollment period shouldn’t feel like a full time job.

You deserve a clear path to the coverage you’ve earned without the high pressure sales tactics. This 2026 Florida calendar provides a definitive timeline of every critical window, ensuring you avoid costly mistakes and secure the extra benefits you need. We’ll help you identify which specific enrollment period applies to your current life stage and how to connect with a licensed Jensen Beach agent for a no obligation review. From the Initial Enrollment Period to the fall Open Enrollment dates, this guide replaces confusion with local expertise and steady guidance.

Key Takeaways

- Identify the specific seven-month window surrounding your 65th birthday to secure your benefits and avoid permanent late-enrollment penalties.

- Distinguish between the Annual Election Period and the Medicare Advantage Open Enrollment Period to ensure your 2026 coverage remains both comprehensive and affordable.

- Master the Florida-specific calendar to understand exactly when is medicare enrollment period for your unique health and financial situation.

- Learn how life events like moving to Florida or losing employer-sponsored insurance can grant you a Special Enrollment Period to update your plan.

- Discover the advantages of a no-obligation review with a local Jensen Beach expert who understands the nuances of the Florida Medicare market.

Understanding the Medicare Enrollment Timeline in Florida

A Medicare enrollment period is a specific window of time when you can join, switch, or drop your healthcare coverage. Knowing exactly when is medicare enrollment period for your unique situation is the only way to avoid gaps in care. Florida residents have specific dates to track in 2026, and missing these deadlines can result in higher monthly premiums that last for the rest of your life. Understanding the Medicare Enrollment Timeline helps you distinguish between federal requirements and private plan options.

In Jensen Beach and across the Treasure Coast, your choices often come down to Original Medicare (Part A and B) managed by the federal government or private plans like Medicare Advantage. While Part A and B provide a foundation, many seniors opt for private plans to secure extra benefits like dental or vision coverage. To better understand how these windows work, watch this helpful video:

For the 2026 calendar year, most Florida seniors will encounter four primary enrollment windows:

- Initial Enrollment Period (IEP): The 7-month window surrounding your 65th birthday.

- Annual Enrollment Period (AEP): Running from October 15 to December 7, this is when you can change your 2026 coverage.

- Medicare Advantage Open Enrollment Period (MA OEP): From January 1 to March 31, specifically for those already enrolled in an Advantage plan.

- Special Enrollment Periods (SEP): Triggered by life events, such as moving to a new zip code in Florida or losing employer coverage.

Why Florida Seniors Often Miss Deadlines

Many seniors in the Sunshine State find themselves overwhelmed by the sheer volume of mailers and TV ads that arrive every fall. Local marketing often blends official CMS dates with private plan promotions, which creates confusion about when is medicare enrollment period for their specific needs. It’s vital to focus on your “Medicare Birthday,” which is the three-month period before and after you turn 65. If you’re turning 65 soon, our licensed agents can help you map out these dates to ensure you don’t miss your initial window. Missing this window often means waiting until the next General Enrollment Period, leaving you without coverage for months.

The Cost of Waiting: Late Enrollment Penalties

Waiting too long to sign up isn’t just a minor mistake; it’s an expensive one that impacts your fixed income. The Part B penalty is a 10% increase for every 12-month period you were eligible but not enrolled. This penalty is added to your monthly premium permanently, meaning you pay more for the exact same coverage as your neighbor. For residents in Martin County, you must also ensure you have “creditable coverage” for prescription drugs. If your private plan or former employer coverage doesn’t meet CMS standards, you could face a Part D penalty as well. Speaking with a local expert provides the peace of mind that your 2026 enrollment is handled correctly and efficiently.

The Initial Enrollment Period (IEP): Your First Opportunity

Understanding when is medicare enrollment period for the first time starts with your 65th birthday. This specific window, known as your Initial Enrollment Period, lasts exactly seven months. It includes the three months before your birth month, the month you turn 65, and the three months following. Missing this window can lead to permanent late-enrollment penalties. These penalties increase your monthly Part B premiums by 10% for every 12-month period you were eligible but didn’t sign up.

To ensure a smooth transition, follow these four steps. First, determine if you’ll be automatically enrolled. If you’ve received Social Security benefits for at least four months before turning 65, the government typically mails your Medicare card automatically. Second, if you’re still working in Florida, evaluate your need for Part B. You might delay this if you have qualifying employer coverage. Third, compare Jensen Beach Medicare Advantage vs. Supplement plans. Advantage plans often include extra benefits like dental and vision, while Supplements offer predictable costs. Finally, confirm your enrollment dates. Signing up during the first three months of your IEP ensures your coverage begins the first day of your birth month.

Turning 65 in Jensen Beach: A Local Checklist

Living on the Treasure Coast means you have access to specific provider networks. You must verify that your preferred local doctors and specialists are part of the network before selecting a plan. The first three months of your IEP are the most critical for avoiding coverage gaps. You can explore your turning 65 medicare options to see which local plans offer the best value for your specific health needs and budget.

Working Past 65 in Florida

Many Florida residents continue working well past age 65. If your employer has 20 or more employees, your group health plan is usually primary. This means you might be able to delay Part B without a penalty. You must ensure your employer coverage is considered “creditable” under federal guidelines. When you eventually retire, you’ll trigger a Special Enrollment Period. This eight-month window allows you to sign up for Part B without late fees. If you’re unsure about your current coverage status, you can speak with a local expert for a quick, no-obligation review of your situation.

Annual Enrollment vs. Open Enrollment: Clearing the Confusion

Many seniors find themselves asking when is medicare enrollment period because the terminology often overlaps. There are two distinct windows you need to track to ensure your 2026 coverage remains affordable and effective. The Annual Election Period (AEP) occurs every fall, while the Medicare Advantage Open Enrollment Period (MAOEP) serves as a follow-up window in the spring. Understanding the specific rules for each prevents gaps in your healthcare and protects your peace of mind.

The October 15 Deadline: Your Chance to Switch

The AEP runs from October 15 through December 7 every year. This is the most flexible time of the year for Florida residents. During these seven weeks, you can move from Original Medicare to Medicare Advantage plans, switch between different Part C providers, or adjust your Part D prescription drug coverage. It’s the only time most people can make these broad changes without needing a qualifying life event.

Your preparation should begin in September when Florida carriers mail out the Annual Notice of Change (ANOC). This document is essential for 2026 planning. It outlines exactly how your premiums, co-pays, and drug formularies will shift in the coming year. Since many Florida plans are adjusting their provider networks for 2026, a no-obligation review with a licensed agent ensures your current doctors are still participating. If they aren’t, the December 7 deadline is your final chance to secure a plan that includes your preferred providers for the full calendar year.

The January 1 – March 31 Window: A Second Chance

If you discover your new plan doesn’t meet your needs after January 1, the MAOEP offers a specific safety net. This window is only available to those who are already enrolled in a Medicare Advantage plan. You cannot use this period to switch from Original Medicare to a Part C plan for the first time. Knowing exactly when is medicare enrollment period for these specific changes helps you avoid being locked into a plan that doesn’t fit your budget. During this time, you have two primary options:

- Switch to a different Medicare Advantage plan.

- Drop your Medicare Advantage plan and return to Original Medicare.

If you choose to return to Original Medicare during this time, you can also join a separate Medicare prescription drug plan. For a retiree in Jensen Beach who realizes their new 2026 plan doesn’t cover a specific local clinic, this window is a vital opportunity to correct that mistake. Our local experts provide the clarity you need to compare these options, ensuring you don’t lose coverage or face unexpected costs during the transition.

Special Enrollment Periods (SEP) for Florida Life Events

Life doesn’t always follow a set calendar. You might find yourself asking when is medicare enrollment period if you miss the standard fall window due to a major life change. Special Enrollment Periods (SEPs) act as a safety net for Florida seniors facing specific transitions. These windows typically last 60 days from the date of your qualifying event, though some timelines vary based on the situation.

- Losing Employer Coverage: If you work past 65 and finally decide to retire, you have an 8-month window to sign up for Part B. However, you only have 2 months to join a Medicare Advantage or Part D plan once your group coverage ends.

- Qualifying for Extra Help: Low-income Florida residents who receive the Low-Income Subsidy (LIS) can change their drug or Advantage plans once per calendar quarter during the first nine months of the year.

- FEMA-Declared Emergencies: Florida is no stranger to major weather events. If a hurricane or tropical storm results in a FEMA emergency declaration, CMS often grants an SEP for affected residents who were unable to make changes during a regular enrollment window.

Relocating to the Treasure Coast

Moving to Jensen Beach or Stuart is an exciting transition, but it requires immediate attention to your healthcare. Your previous HMO or PPO plan from a state like New York or Ohio won’t work in Martin County because Medicare Advantage networks are zip-code specific. You must notify Medicare of your move to trigger a 2-month SEP. This window allows you to select a local network that includes providers at Cleveland Clinic Martin North or specialized clinics in the Treasure Coast area. Choosing between a local HMO or a flexible PPO depends on your preferred doctors in the Florida market.

Chronic Conditions and D-SNP Eligibility

Seniors managing specific health challenges don’t have to wait for October to find better support. If you’re diagnosed with a chronic condition like diabetes or chronic heart failure, you may qualify for a Chronic Special Needs Plan (C-SNP). Additionally, those who are “dual eligible” for both Medicare and Medicaid can access Dual Special Needs Plans (D-SNP). These plans often allow for enrollment flexibility outside the standard when is medicare enrollment period questions that most seniors face. Selecting the best Medicare Advantage plans for these conditions provides targeted benefits like $0 insulin copays or transportation to medical appointments.

Are you unsure if your recent life change qualifies for a special window? Speak with a local expert for a no-obligation review of your current eligibility.

How to Enroll with a Jensen Beach Medicare Expert

Choosing your health coverage shouldn’t feel like a transaction with a stranger in a distant call center. National toll-free numbers often route you to agents who have never stepped foot in Martin County. These representatives might not realize that a specific plan lacks a robust network at local facilities like Cleveland Clinic Martin North. Working with a local expert provides a layer of security that a generic hotline cannot match. You get clear answers from someone who understands the Jensen Beach healthcare landscape intimately.

When you prepare for your no-obligation Medicare review in 2026, bring your Red, White, and Blue Medicare card along with a complete list of your current prescriptions. Having your dosage levels and frequencies ready allows your agent to run an accurate cost analysis. We sit down with you to compare Florida Blue, Humana, and UnitedHealthcare, looking specifically at how their 2026 co-pays and deductibles impact your bottom line. Once you select a plan, we handle the enrollment paperwork and confirm your 2026 effective dates. You can expect your new member ID card to arrive in the mail within 7 to 14 business days after your application is processed.

Personalized Guidance in Martin County

Face-to-face consultations at our Jensen Beach office eliminate the guesswork that often leads to enrollment errors. We don’t just look at premiums; we verify that your specific Jensen Beach doctors and specialists are actively participating in the plan’s network for the upcoming year. Florida Medicare Advantage agents are licensed to represent multiple top-rated carriers, which means our loyalty stays with you rather than a single insurance company. This local perspective ensures you don’t lose access to the providers you’ve trusted for years.

Your Next Steps for 2026 Coverage

The best time to secure your health future is before the deadlines approach. Scheduling your free plan comparison today gives you the luxury of time to weigh every option without pressure. Knowing exactly when is medicare enrollment period allows you to stay ahead of the crowd and avoid the last-minute rush that happens every December. We pay special attention to medicare part d plans to protect you from future drug cost surprises. Our goal is to ensure your 2026 coverage provides both the medical benefits you need and the peace of mind you deserve.

- Review: Analyze your current 2025 usage to predict 2026 needs.

- Compare: Evaluate at least three different carrier options side-by-side.

- Confirm: Verify pharmacy networks and tier-level pricing for all medications.

- Finalize: Submit your 2026 application with a licensed professional to ensure accuracy.

Take Control of Your Florida Medicare Timeline

Navigating the 2026 calendar requires more than just marking dates. You’ve learned that your Initial Enrollment Period spans a strict 7-month window centered around your 65th birthday. You also know the Annual Enrollment Period runs from October 15 through December 7 every year. Missing these deadlines can lead to a 10% Part B penalty for every 12-month period you delayed. Understanding exactly when is medicare enrollment period ensures you don’t lose access to essential benefits or face unexpected monthly costs.

As a Licensed Florida Insurance Agency with a local Jensen Beach office, we help you compare options from top-rated carriers like Humana, UnitedHealthcare, and Florida Blue. You don’t have to decipher complex federal guidelines alone. Our team provides the clarity you need to choose a plan that fits your specific health needs and fixed budget. We’re here to act as your steady guide through every regulatory change. Reach out today to secure your coverage and gain the peace of mind you deserve.

Schedule Your No-Obligation 2026 Medicare Review with a Local Jensen Beach Expert

We look forward to helping you navigate your healthcare journey with confidence and ease.

Frequently Asked Questions

When is the Medicare open enrollment period for 2026?

The Medicare Annual Enrollment Period for 2026 coverage runs from October 15, 2025, through December 7, 2025. During these 54 days, Florida residents can join, switch, or drop a Medicare Advantage or Part D plan. Your new coverage then begins on January 1, 2026. This is the primary window for most seniors to adjust their benefits and ensure they have the lowest co-pays for the coming year.

Can I change my Medicare Advantage plan at any time in Florida?

You cannot change your Medicare Advantage plan at any time; you must use specific windows like the Open Enrollment Period from January 1 to March 31. During these 90 days, you can make a one-time switch to a different Advantage plan or return to Original Medicare. Outside of this and the fall AEP, you generally need a qualifying life event to make changes. Speaking with a local expert can help you determine if you qualify for a 60-day Special Enrollment Period.

What happens if I miss my Initial Enrollment Period at age 65?

If you miss your 7-month Initial Enrollment Period, you may face a permanent late enrollment penalty of 10% for every 12-month period you were eligible but didn’t sign up for Part B. You’ll also have to wait until the General Enrollment Period to apply. This delay could leave you without coverage for several months. Our licensed agents can help you calculate these costs during a no-obligation review to minimize your financial impact.

Is there a special enrollment period if I move to Florida from another state?

Yes, moving to Florida qualifies you for a Special Enrollment Period that typically lasts for 2 full months after the month you move. This 60-day window allows you to choose a new plan that fits the local Florida provider networks. If you notify your plan before you move, your chance to switch begins the month before you move and continues for 2 months after. It’s a vital time to secure peace of mind in your new home.

How long does the Medicare General Enrollment Period last?

The Medicare General Enrollment Period lasts for 3 months, running from January 1 through March 31 each year. If you missed your initial chance to sign up, this is your annual opportunity to enroll in Part A or Part B. Coverage requested during this time becomes effective the first day of the month after you sign up. Knowing when is medicare enrollment period for general sign-ups helps you avoid longer gaps in your medical protection.

Can I switch from Medicare Advantage to a Supplement plan during AEP?

You can switch from Medicare Advantage to a Supplement plan during the Annual Enrollment Period, but you’ll likely need to pass medical underwriting in Florida. Unlike Advantage plans, Medigap insurers can deny coverage based on your health history if you’re outside your initial 6-month Medigap Open Enrollment window. A licensed agent can review your 2026 options to see if you meet the 100% health requirements for a specific Supplement provider.

Do I need to re-enroll in Medicare every year?

You don’t need to re-enroll in Medicare every year because your current coverage usually renews automatically on January 1. However, insurance companies often change their drug formularies and provider networks annually. Reviewing your Annual Notice of Change (ANOC) each September is essential. We recommend a no-obligation review every October to confirm your current plan still offers the best savings for your specific prescriptions and doctor visits.

What is the “Medicare Birthday” rule for Florida residents?

Florida doesn’t have a formal “Birthday Rule” like California, but residents have a 6-month Medigap Open Enrollment Period starting the month they turn 65. During this 180-day window, you have a guaranteed right to buy any Medigap policy sold in Florida regardless of health conditions. Once this period ends, you might face medical questions to change plans. Understanding when is medicare enrollment period for your specific birth month ensures you get the lowest possible premiums.